US inflation: A fascinating and unique moment for investors - Firstlinks newsletter

+ Hamish Douglass explains and warns; Don Stammer X-Factor; Noel Whittaker 10 tips; Big global trends for 2022; Sell home for aged care; Fixed interest.

Inflation ... it seems such a dry subject and Firstlinks does not normally spend much time on a macro theme, but this is a fascinating and unique moment. The US CPI is up 6.8% in the last 12 months but the 10-year US bond is holding at around 1.5%, pushing the real yield to an unprecedented minus 5.3%. Central bankers are responding. US Fed Chair Jerome Powell and the Reserve Bank's Philip Lowe fear inflationary expectations are becoming baked into prices and wages. Powell said in 2018 of the Federal Open Market Committee (FOMC):

"The reality or expectation of a weak initial response could exacerbate the problem. I am confident that the FOMC would resolutely ‘do whatever it takes’ should inflation expectations drift materially up or down or should crisis again threaten."

'Do whatever it takes' in raising rates is a big change for a central banker who has been waiting for firm evidence before moving. For most of his first term, Powell (like Lowe) wanted to see inflation higher, which he referred to as 'achieving the goal'. He would be happy to see it settle anywhere from 2% to 3%.

Overnight, the Fed doubled the pace of bond tapering and forecast three rate hikes in 2022 and another three in 2023. The Fed noted that:

“supply and demand imbalances related to the pandemic and the reopening of the economy have continued to contribute to elevated levels of inflation”.

Powell said the Fed Funds rate increases could start as early as March 2022 as there is a "real risk high inflation becomes entrenched".

Meanwhile, as this screenshot from the AFR this week shows, the stockmarket was not worried about the high CPI number as it pushed to a record high. It's a remarkably sanguine view.

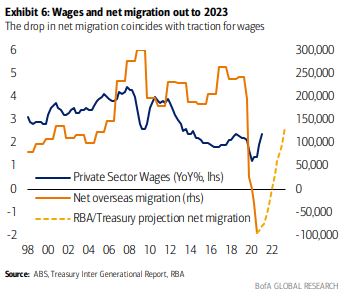

In Australia, the drop in immigration has encouraged a rise in wages, as the chart below shows. Expectations are that a return of net migrants towards the recent norm of 200,000 or more a year would have the reverse effect, and reduce the pressure on rising rates. This is why Omicron is so important for inflation, as case and hospital numbers may threaten the return of foreign labour.

So inflation, wages, the virus and house prices are all linked, and Hamish Douglass gives some important warnings in our edited transcript of his presentation to Stanford Brown clients this week. Douglass touches on some issues at Magellan that have made headlines this week, including explaining underperformance, but it is his worries about the virus and inflation, plus a black swan of a Middle East war, which are most important for investors. He shows why conditions are so dangerous and the markets are 'playing with fire':

"We're watching this party of the century occurring at the moment and I feel like the person who is failing the ID check at the door."

Meanwhile, Social Services Minister Anne Ruston announced this week that the Pension Loan Scheme would be renamed the Home Equity Access Scheme with a couple of important tweaks: from 1 January 2022, the interest rate will fall from 4.5% to 3.95%, and from 1 July 2022, lump sums of $12,000 a year for singles and $18,000 for couples can be drawn. The name change is good because the scheme is open to Australians aged 66 and over who own residential property and not only those on the age pension.

And just when it seemed falling auction clearance rates might deliver some respite for prices and the next generation of buyers, CoreLogic produced this chart showing a lift in mortgage activity:

"CoreLogic systems monitor more than 100,000 mortgage activity events every month across our four main finance industry platforms ... the Mortgage Index provides the most timely and holistic measure of mortgage market activity available."

The pandemic has accelerated many trends, particularly in tech, creating faster growth paths for some companies. Shannon McConaghy identifies three companies benefitting from such changes. But there is less focus on the other side, where the market is expecting pandemic patterns to continue, and two of these are identified as shorting (selling) opportunities. That's one of the strengths of managing a long/short portfolio.

Two articles from legends of Australian financial markets with well over 100 years in markets between them. For 40 of those years, Don Stammer has been recording the market's annual X-Factor ... the big issue of the year likely to have a major impact next year, and he also shows his full 40 year list. Lots of issues long since considered irrelevant. Then Noel Whittaker explains why financial advice is worthwhile for all retirees, as he describes some little-known rules that could be costly if ignored.

Still on great hints for later in life, Rachel Lane analyses the claim that people need the proceeds from their house sale to pay for aged care services. Owning a home has many advantages and selling it may not be the best strategy.

Fixed interest funds may seem like the poor cousins of equity funds, with less of the glamourous stock stories and elevated returns in booming markets. But as Andrew Cummins and David Hutchinson show, many investors and financial advisers still rely on a core group of fixed interest funds for their income, capital protection and diversity, and they reveal the funds that have identified what these investors need.

Then James Abela and Maroun Younes reveal the global themes they follow in managing a portfolio of mid-sized companies where the investible universe is immense. What do they look for to whittle down the almost unlimited choices?

Going back a couple of weeks, an article on green hydrogen by Michael Collins drew many comments, including an expansion of the ideas by Allan Blood. The technology becomes even more relevant when we read this week that our truck transport system depends heavily on diesel topped up with AdBlue, which uses urea, most of which comes from China. We are learning more about our dependency on fragile global supply chains, another subject that Hamish Douglass covers.

And I was struck by a comment by Harold Mattner on my article on the stocks I expect to own for decades despite my market pessimism:

"Thanks Graham for all your articles…thoroughly enjoyable and useful. I lost money for the first twenty years of investing, and reached a stage where I had to change, or give it up. I found investing was an extension of who I was as a person, so to change oneself before I could change my investing style was quite an insight."

This week's White Paper from Antipodes is a quick read with useful charts on the global outlook for 2022, noting the impact of the withdrawal of stimulus, the threat of inflation and a few surprises.