Loud and clear: covid crisis a shot in the arm for Zoom

The shutdown has made the videoconferencing platform a mainstay of life and its quarterly numbers have a very nice ring to them

Mentioned: Zoom Communications Inc (ZM)

Forget the connection woes and the online saboteurs. Zoom (ZM), the videoconferencing provider that has been a defining feature of the covid crisis, has dialled in with a stellar first quarter result, which Morningstar analyst Dan Romanoff says is the best quarterly performance by a software company he’s seen in two decades.

Romanoff has increased his fair value estimate for the no-moat company from US$62 to US$116, and says it has addressed lingering security problems and is primed for growth, even if the current valuation is hard to justify, especially given the company’s high data costs.

“With no hint of exaggeration, this is the strongest relative quarter we have seen in 20 years of software coverage,” Romanoff said in a note on Wednesday.

“We see a long runway for growth as the company gains traction with its Zoom Phones solutions as well, and we are impressed by management’s ability to drive strong growth while also delivering on the bottom line—to put it mildly.”

Zoom has about 265,400 customers and at its April peak had 300 million daily meeting participants. It came under fire earlier this year after widespread reports of “zoombombing” whereby people managed to gatecrash calls and interject pornographic images and other interruptions.

The company has, however, tightened its security and has won back high-profile customers it had lost such as the New York City Public School System.

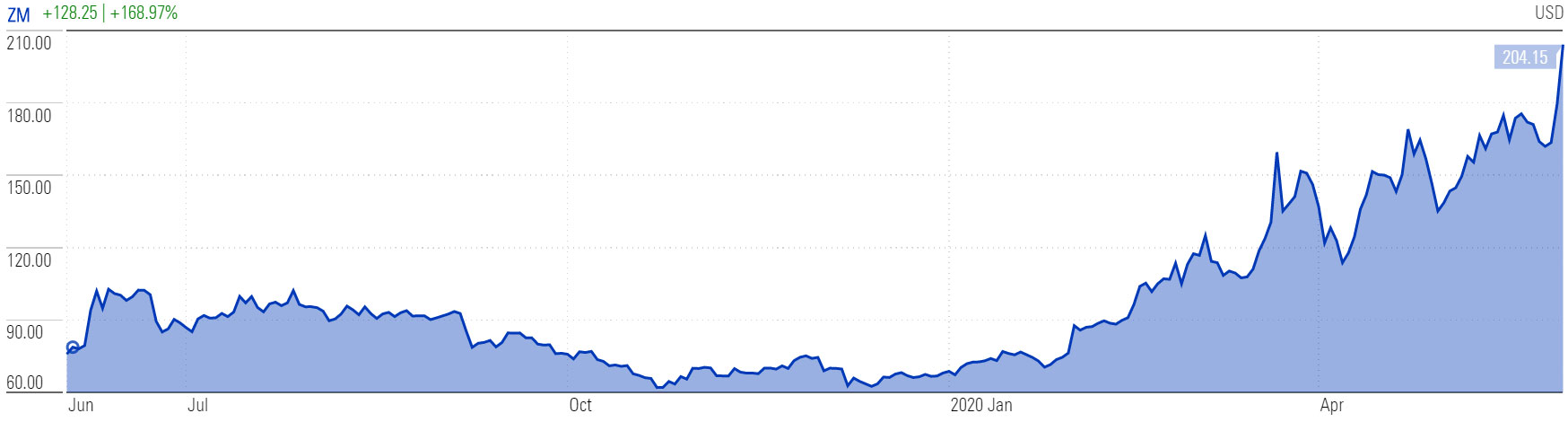

When Zoom listed last year it had a market cap of US$15.9 billion. That now stands at more than US$58 billion. It’s share price has tripled this year, going from US$68.72 on 2 January to US$208 overnight.

“We are in uncharted territory model-wise after huge quarterly upside in the face of the COVID-19 recession along with sharply higher guidance, which in turn drives our new fair value estimate from $62 to $116,” Romanoff says.

“We note shares have approximately tripled year to date thus far, so even allowing for a complete model reset, we still cannot come close to supporting the current share price within the context of our discounted cash flow model.”

Stock Price | Zoom (ZM), 1 Yr

Source: Morningstar Direct

The company raised its full-year revenue forecast to a range of US$1.78 billion to US$1.80 billion from US$905 million to US$915 million. Analysts on average expected revenue of US$935.2 million for the fiscal year ending January 2021.

Revenue grew 169 per cent year over year to US$328 million, eclipsing the US$200 million guidance midpoint as well as Romanoff’s generally in-line US$202 million estimate.

Demand for Zoom’s products remains robust as the company continues to gather new customers. Romanoff says he shares management’s enthusiasm for Zoom Phones, which he thinks will boost revenue over the next several years as more features are added and reference accounts are established.

“Given the step function in the financial model, we think Zoom’s opportunity is immediately larger, especially given that the company’s go to market strategy for Zoom Phones is to target its existing customer base.

“To that end, customers with more than U$100,000 in trailing annual revenues grew 90 per cent year over year to 769. Zoom disclosed it added more than 500 customers with more than US$100,000 in annual recurring revenue during the quarter. Clearly larger customers added meaningfully to their seat count.”

Despite the revenue boost, Zoom’s costs are rising and the boom in usage may be tapering as economies get back to life. The company says the April peak usage of 300 million daily meeting participants dipped in May although they expect it to regain 300 million.

The company’s cost of revenue was up 330 per cent to US$103.7 million, which lowered its gross margin to 68.4 per cent from 80.2 per cent a year earlier.

A key overhead is data centres and the bandwidth to host calls. Zoom has its own data centres, but must also pay for cloud computing services from Amazon.com, Amazon Web Services and Microsoft, and in April added Oracle Corp as a vendor.

Zoom’s rivals include Cisco Systems Inc’s Webex, Microsoft’s platform Teams and Google’s Meet platform for paying customers, particularly businesses.