Covid-19 and the future of financial planning

It’s time to rethink what our financial goals can and should look like, writes Morningstar director of personal finance Christine Benz.

Just five short months after its abrupt slide into bear-market territory at the outset of the coronavirus pandemic, stock market indexes had regained their lost ground and begun to scale new highs by late August 2020.

But the market’s speedy recovery is dissonant with a still-struggling economy. In addition to wreaking havoc on the economy at large, the pandemic has had sudden and significant repercussions for how individuals conduct their financial planning—specifically, how they approach spending and saving goals.

Many households have experienced income shocks and have burned through their cash reserves, illustrating the critical role that liquid assets play in the health of any financial plan. The pandemic’s economic side effects also have significant implications for when and how older adults plan their retirements. Not only have older workers experienced some of the highest rates of job loss of any age band, but in previous recessions, it has also taken older unemployed workers a much longer time to become re-employed than younger ones. That, plus the fact that a recovering stock market has lifted retirement account balances, has no doubt prompted some to ponder early retirement. Yet low interest rates—while a boon to borrowers—are a headwind for people nearing or in retirement.

All of these trends have implications for the way households—and the advisors who assist them—manage their finances. While the COVID-19 crisis has brought these topics to the forefront, their importance is likely to persist post-pandemic as well.

Chapter 1: How the pandemic has impacted financial planning for emergencies

The economic shock related to the pandemic illustrates, yet again, the importance of emergency reserves as part of a financial plan and the difficulties that many individuals and households face in amassing these “rainy-day funds.”

Lower-income households, not surprisingly, are the least well equipped to handle financial emergencies. But the lack of short-term financial wherewithal isn’t limited to lower income tiers.

It’s a wise practice to have an emergency fund separate from long-term assets. Withdrawing from retirement accounts is suboptimal because those withdrawn funds can’t benefit from market appreciation—imagine, for example, the worker who liquidated stocks from a retirement account in late March 2020, only to miss the subsequent recovery.

Plus, an emergency fund can boost peace of mind and financial confidence in long-term goals. In a report conducted by AARP, people with emergency funds felt 2.5 times more confident in their ability to achieve their financial goals than those who did not. Financial advisors can play a role in helping clients set a savings goal for these emergency funds based on factors like their employment status (contract or permanent), variability of earnings, number of earners in the family, and so on.

- Gig economy and contract workers are naturally at risk for more frequent and longer work interruptions than permanent workers and therefore should prioritise building emergency funds larger than the standard benchmark of three to six months’ worth of living expenses.

- Higher-income workers and/or those with more specialized career paths should also target larger emergency funds, because such positions typically take longer to replace than lower-income, less specialized jobs.

- Dual-income households arguably need less of an emergency reserve than single-earner households, because the probability of both earners facing job loss at once is less than it is for single earners.

The fact that so many consumers struggle with amassing emergency reserves may also reignite interest among policymakers in allowing employers to offer so-called “sidecar” funds. The idea behind such funds would be for employees to contribute aftertax money automatically to an emergency fund. Once cash builds up to the employee’s own target, she could direct future pretax contributions to long-term retirement savings.

Automating these contributions through payroll deductions may make it easier for individuals to save than when they’re saving on a purely discretionary basis.

Chapter 2: How older workers can approach financial planning for potential early retirement

In addition to its impact on emergency savings and healthcare spending, the current economic crisis will likely have implications for retirement planning for many individuals. Contrary to the financial crisis of 2007-09, when older adults maintained higher levels of employment than younger cohorts, the COVID-19 crisis has thus far had a disproportionate effect on older workers.

While some of these newly unemployed older adults may be assessing whether they can replace the jobs they've lost, a segment of them may also be mulling whether an early retirement is an option. At the same time, it’s worth noting that early retirement isn’t exclusively a bear-market/recessionary phenomenon. Research conducted by Morningstar’s David Blanchett concluded that workers often retire earlier than they expected to—about four years earlier, on average.

But early retirement isn’t always in an individual’s best interest—rather, working even a few years longer than the traditional retirement age of 65 can be hugely beneficial to the health of a retirement plan, and early retirement can pose challenges to a plan’s sustainability. For instance:

- Early retirement can truncate opportunities for additional retirement-plan contributions, compounding, and tax deferral.

- Withdrawals over a longer time horizon can force a lower withdrawal rate or reduce the probability that the retiree’s funds will last over his/her time horizon.

Of course, the decision about when to retire is about much more than money. The employee’s own health and that of his/her family members, longevity considerations, the physical and mental strains of their job, and, of course, economic conditions may also be in the mix. But financial advisors can help their clients understand the trade-offs associated with early retirement, and in particular the stresses that may impact the viability of the financial plan.

On the flip side, the pandemic’s drive toward remote work could make staying employed easier and more attractive for older adults who wish to continue working, are able to do so, and can take advantage of flexible work arrangements. For example, working longer may be more palatable if it doesn’t entail a commute or if the older worker can live where he or she eventually retires.

Chapter 3: How can you accommodate low yields in a financial plan?

Finally, retirees of all ages—early or otherwise—have a huge challenge today in the form of very low bond yields, the result of activity designed to ignite an economy that would otherwise be struggling even more amid the pandemic-related slowdown.

To be sure, low yields aren’t a complete negative for retirees’ financial plans. They’re a big plus for borrowers, a group that increasingly includes retirees. Swapping into a lower-rate or shorter-term mortgage or buying a car with a very low or even 0 per cent interest rate could reduce in-retirement expenses for many individuals. Moreover, the fact that safe securities yield so little today has contributed to the ascent of higher-risk assets, especially stocks.

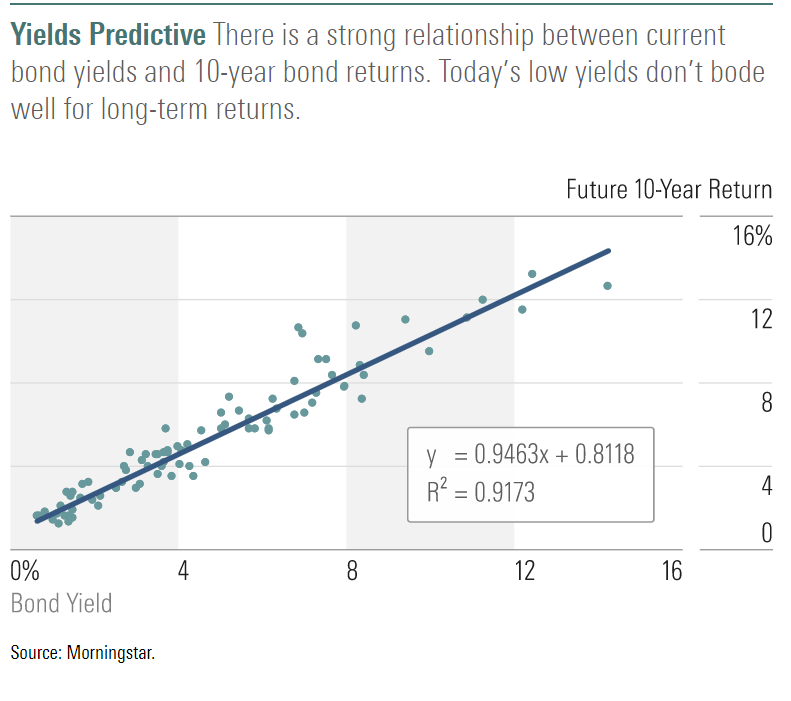

But even as retirees have gained on one side of the ledger as yields have declined, they’ve lost on the other. Not only do low yields reduce how much retirees can wring from their safe investments, but yields are also predictive of what bonds are apt to return over the next decade.

Investors aren’t even able to find a bump in yields today when they venture way out on the risk spectrum—either by accepting more interest-rate sensitivity or credit risk—even though they are subject to a substantially higher level of volatility. Long-term high-quality bonds yield just over 2 per cent today, whereas corporate bonds are yielding just over 3 per cent. In other words, every rock has been turned over in search of yield.

These low yields constrain the return potential of portfolios that have an allocation to bonds and cash, at least for the next decade. That has implications for withdrawal rates, in that what’s considered sustainable over a retiree’s own time horizon depends completely on the returns of that portfolio’s constituent holdings. Assuming even a generous 2 per cent return for fixed income and an equally generous 6 per cent equity return, a 60 per cent equity/40 per cent bond portfolio would return just 4.4 per cent over the next decade.

That suggests that new retirees, in particular, should be conservative on the withdrawal rate front, especially because the much-cited “4 per cent guideline” for portfolio withdrawal rates is based on market history that has never featured the current combination of low yields and not-inexpensive equity valuations. Morningstar’s Blanchett and retirement researchers Michael Finke and Wade Pfau co-authored research in 2013 suggesting that low yields conspire against the viability of the 4 per cent guideline.

The equity market “bailed out” low yields over the past decade, but Pfau thinks the odds are stacked against 4 per cent as a sustainable withdrawal rate for new retirees, especially given that starting equity valuations are not cheap.

Finally: Where changes to financial plans will and won’t endure

Some of the spending and saving behaviours brought on by the pandemic could prove fleeting: For example, many households that have maintained employment through this period have been able to increase their savings rates and reduce debt. While those gains are encouraging, they may prove short-lived when the economy has fully reopened and all spending opportunities are back in full force.

The trends outlined above, however, appear to have more staying power. That’s because they were already well in play before the pandemic; the COVID-19 crisis has simply helped accelerate them. While topics like paying for healthcare and low yields on safe securities were likely already top of mind for financial advisors and their clients, they’re even more pressing—and even more deserving of troubleshooting in financial plans—today.

Editor's note: This article was originally published for a U.S. audience on Morningstar.com