Enviro-conscious investors need to cast a broader net

Australian companies do a good job of managing carbon risk, but the country as a whole still trails many developed markets.

Mentioned: Russell Invmts Low Carbon Glb Shrs A (43500), IFP Global Franchise Fund (12160), Australian Ethical Intl Shr (17618), Australian Ethical Balanced (1863), Hyperion Australian Growth Companies (3344), Australian Ethical Income (4766), BHP Group Ltd (BHP), Russell Inv Australian Rspnb Inv ETF (RARI)

Australian investors mindful of environmental considerations are better served offshore than locally, a new Morningstar report shows.

The coronavirus pandemic is a stark reminder of international connections and the systemic risks and vulnerabilities that accompany this, including economic, social, environmental and governance considerations.

In Australia, this biological disaster followed devastating nation-wide bushfires, which turned the focus on climate change in a profound way.

Released this week, Evaluating Carbon Risk in Managed Funds - An Australian Perspective, uses Morningstar's carbon rating tools to compare "carbon risk" in Australian-based managed funds—both global and local equity strategies.

Source: Morningstar Direct

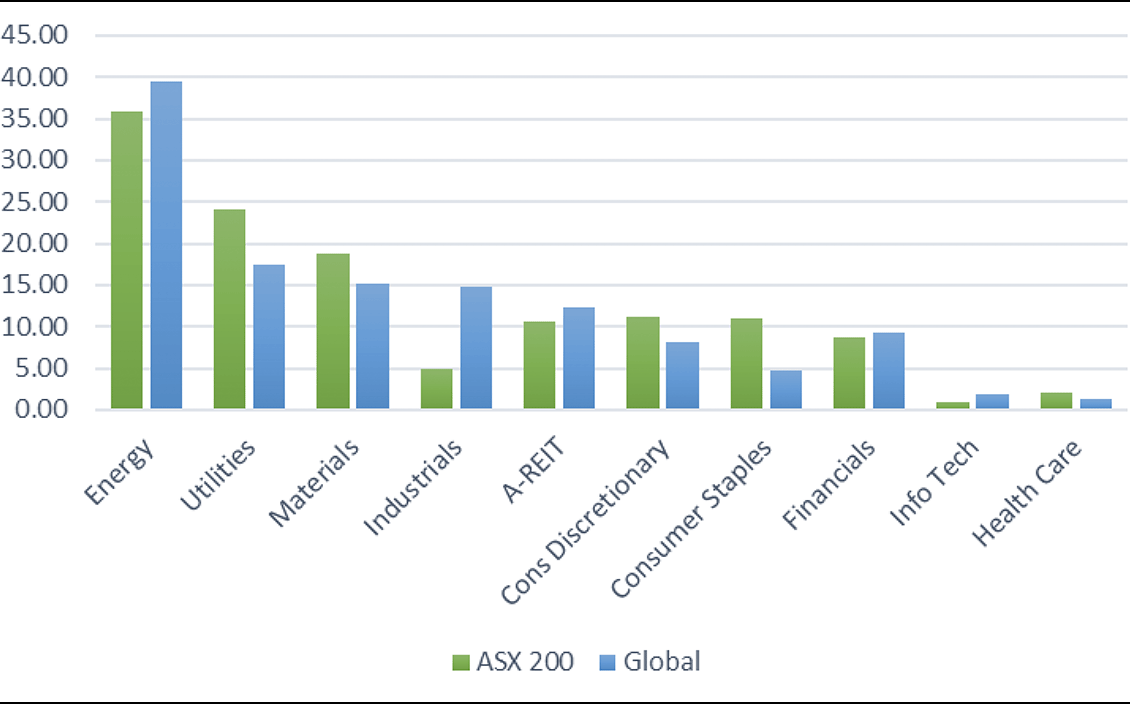

Given that around 40 per cent of the more than 1,850 listed companies on the ASX are energy and materials companies, it's no surprise Australia ranks in a high carbon intensity quintile.

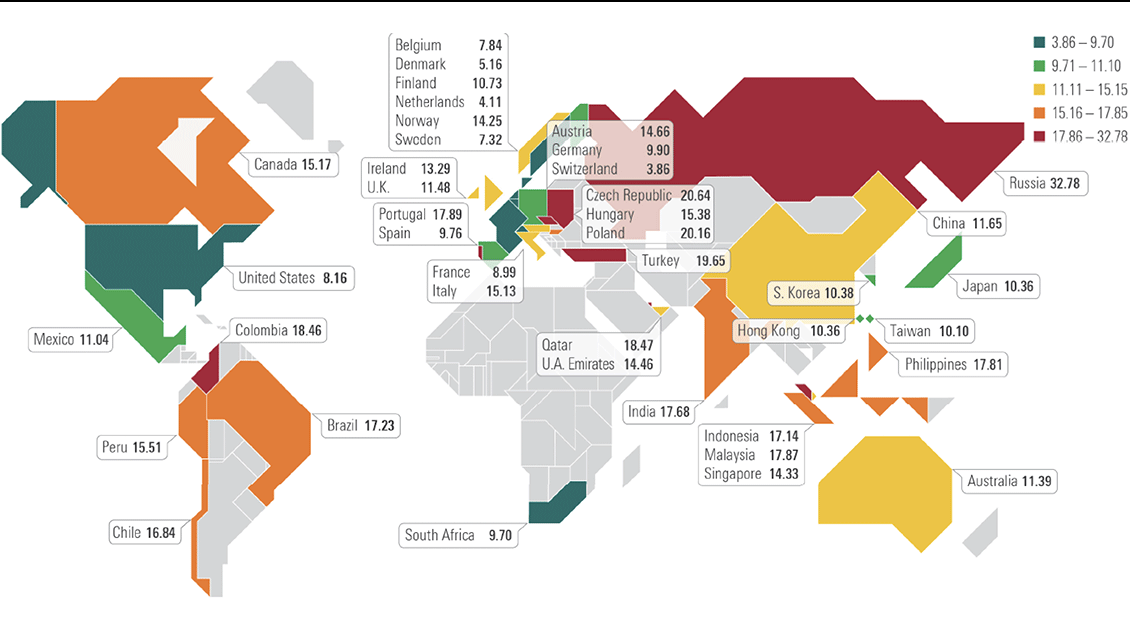

The report indicates that while Australian companies do a good job of managing carbon risk, the country as a whole still trails many other developed markets. Australia scored 11.3 per cent versus 8.6 per cent in the US and an average of 9.4 across Austria, Germany and Switzerland, as shown in the table below.

Source: Morningstar Direct

Among Australian-based large cap domestic equity funds, just 6 per cent receive the Morningstar Low Carbon designation.

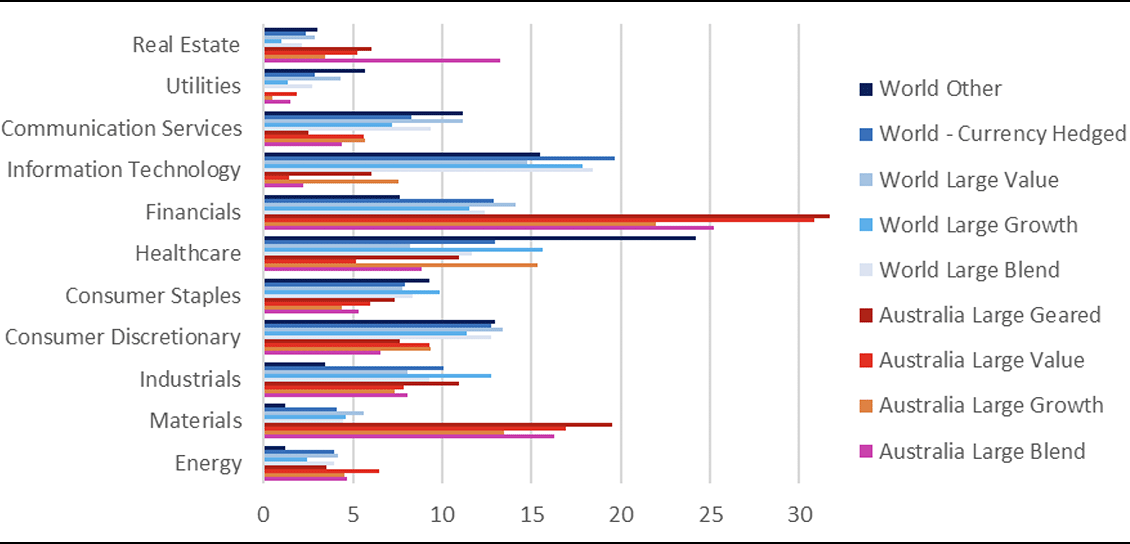

In Australia, large-cap value-focused funds were more likely to be rated Low Carbon—reflecting their higher exposure to financial companies, which have lower carbon risk

This compares poorly with more than 70 per cent of domestic large-growth strategies in Europe and the US. The better carbon score in these countries also reflects the higher exposure to technology and underweight positions in energy companies among their funds

Evaluating carbon risk

Carbon risk is a forward-looking assessment of how companies are tracking as Australia and other markets progress towards becoming low-carbon economies. This metric is calculated by environmental, sustainability and governance rating agency Sustainalytics, which Morningstar acquired earlier this year.

To help investors quickly identify portfolios that are managing carbon risk well, Morningstar now uses the Low Carbon Designation, as shown below. This symbol indicates a fund has a low carbon risk score and low fossil fuel exposure.

In the report, authors Grant Kennaway, director of manager research, and Donna Lopata, manager research analyst, compare the characteristics of Low Carbon Designation funds in Australia with those in other markets.

Hamstrung by policy void

The poor ranking of Australian funds must be viewed alongside Australia's policy framework, which currently has no carbon tax or strictly regulated emissions reduction targets.

While this is a short-term fillip to local companies with high carbon intensity, Sustainalytics cautions the status quo will likely not always be the case.

"This could increase risk over the medium- to long-term, assuming that governments that delay a carbon-reduction policy might have or be forced to enact more stringent regulation in the future," says Sustainalytics.

"Therefore, companies in these regions may risk unpreparedness if they fail to take steps early on and adapt to a carbon-constrained environment."

Source: Morningstar Direct

But there are pockets of opportunity for environmentally focused investors in Australia seeking lower carbon risk domestic equity strategies, despite the smaller numbers relative to global funds.

Sustainable Funds and ETFs

Kennaway notes that Australasian investor money is flowing into active and passive sustainable funds at a roughly equal rate, with the segment attracting inflows of US$310 million in the first quarter of 2020.

Two fund houses—Russell Investments (Russell Inv Australian Rspnb Inv ETF and Russell Invmts Low Carbon Glb Shrs A) and Australian Ethical (Australian Ethical Balanced, Australian Ethical Income and Australian Ethical Intl Shr)—accounted for the majority of inflows for the quarter.

Launches stalling

In terms of new sustainable funds, launches have largely dried up in the Australasian market, after the flurry of launches in 2018 and the first half of 2019. There have been no sustainable fund launches in the first quarter of this year.

Kennaway notes that assets in Australasian sustainable funds dropped in first-quarter 2020, amounting to US$7.94 billion, down from US$10.27 billion at the close of 2019—a decline of 23 per cent.

This compares with a 17 per cent reduction in equity assets—the vast majority of sustainable funds being equity focused—for the overall Australasian fund universe.

The Australian sustainable funds market remains quite concentrated, with the top 10 funds accounting for 54 per cent of total assets in the sustainable fund universe. The largest three funds are the Australian Ethical Balanced fund at just over US$1 billion, the AMP Capital Ethical Leaders Balanced fund at USD 482 million and the Australian Ethical Australian Shares funds with US$439 million.

Accidentally ESG-focused

A key Morningstar finding is that many of the low carbon designated funds aren't explicitly adopting ESG or Low Carbon strategies. According to Kennaway, this indicates Australian investors who conscious target environmentally friendly companies need to dig deeper to find strategies that align with their objectives.

Morningstar's report reveals only one of the Australian equity funds that achieve a Low Carbon Designation, the Perpetual Wholesale Ethical SRI, has an explicit ESG focus.

Despite the absence of a stated climate-aware objective, Hyperion Australian Growth Companies has the lowest carbon risk score of Australian large-equity strategies under analyst coverage. Hyperion's quality and long-term growth focus leads to an overweight position in the healthcare and technology sectors, which have low-carbon risk and virtually no exposure to materials and energy.

While Hyperion Asset Management has a detailed ESG Policy and Framework, its low-carbon risk score was an outcome of the manager's process rather than an intended objective. This highlights the complexities for climate-aware investors in selecting a fund that manages carbon risk.

Pendal Ethical Australian Share, with a carbon-risk score of 12.88 and fossil-fuel exposure of 17.42, is a good example of an Australian large-equity fund under Morningstar coverage that didn’t meet Low Carbon designation requirements, despite the incorporation of ESG in its objectives.

The fund's PDS refers to exclusion of investment in companies mining uranium for weapons manufacture, alcohol or tobacco, gaming, weapons, or pornography. A key point here is that these exclusions have no bearing on carbon risk.

Pendal's strategy seeks exposure to companies offering leading environmental and social practices, products and services—as of 31 March 2020, mining giant BHP (ASX: BHP) makes up more than 5 per cent of that portfolio. While many could consider BHP as having implemented leading ESG programs, the company does not qualify as a low-carbon investment. In fact, Sustainalytics considers BHP at medium carbon risk (score of 19.5). BHP also derives roughly 20 per cent of its revenues from fossil fuels.

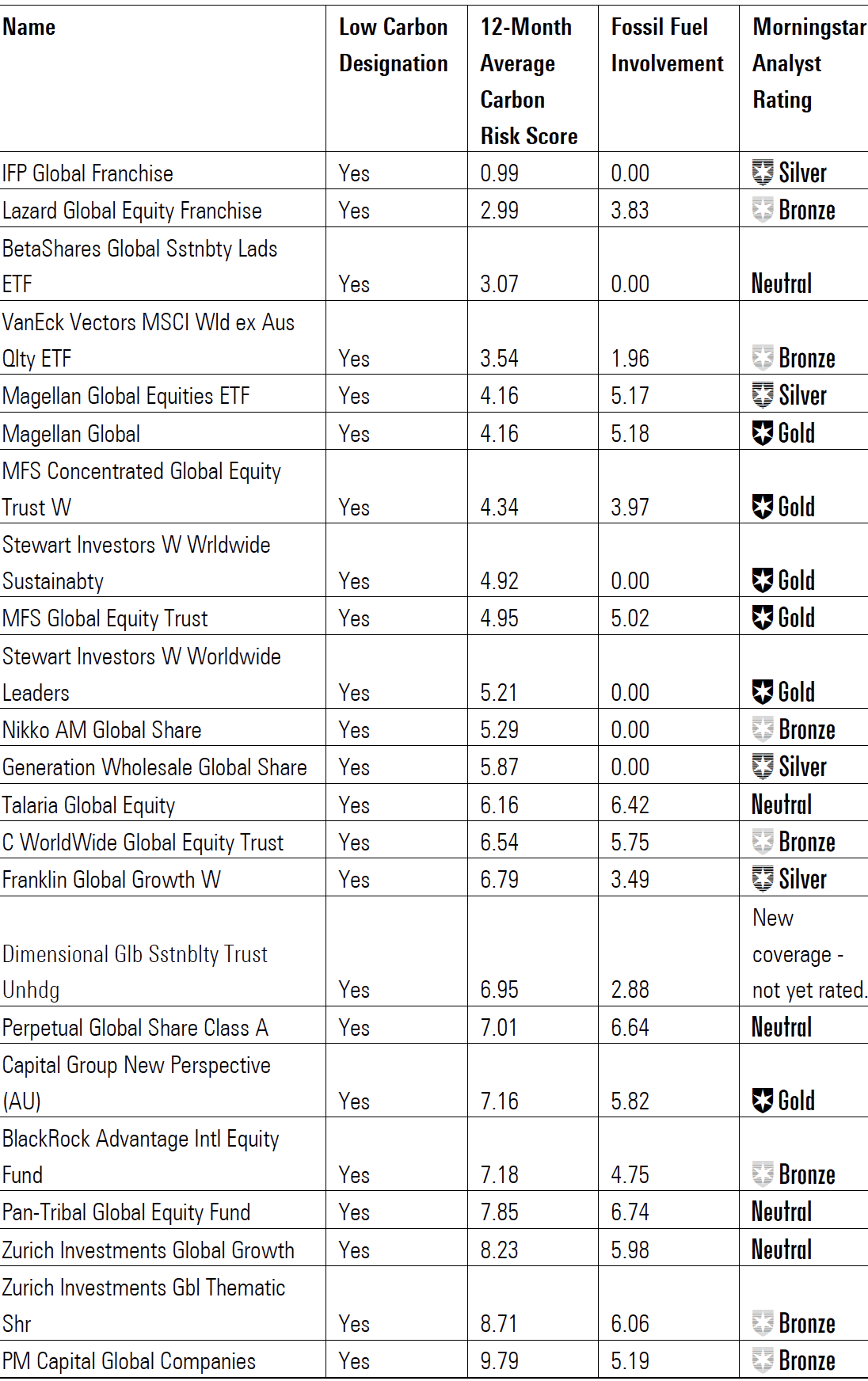

Australian investors have fewer choices of funds with explicitly climate-aware objectives but by using Morningstar’s carbon tools, Kennaway and Lopata identified a set of global large-cap equity strategies that received the Morningstar Low Carbon Designation (listed in order of carbon-risk score).

Twenty per cent of all Australia-domiciled and US-domiciled world large-equity funds received the Morningstar Low Carbon Designation.

IFP Global Franchise, a fund that does not have an ESG-focused objective, receives the lowest carbon-risk score in the world large category. But the authors note that about 5 per cent of the portfolio is invested in British American Tobacco as at 31 March 2020. This highlights the point that the Low Carbon designation is not a measure of broader ESG risks.

Morningstar's carbon metrics are a subset of extensive ESG data available to investors in order to evaluate ESG risks within portfolios. Approaches to sustainable investing are broad, and it is important for investors to understand their nuances and ensure their alignment to a strategy.

Source: Morningstar Direct

Europe continues to lead ESG charge

In comparison, 33 per cent of European-based large-cap global equity funds receive the Low Carbon designation. This supports the view that Europe is at the forefront of climate-aware investing.

Of the 23 funds that made the Australian list, 17 of them (73 per cent) hold Morningstar Medal ratings of either Gold, Silver or Bronze.