Crown takeover: US suitor may need a stronger hand

Blackstone's offer is low, and it must prove it can operate the licence for the narrow-moat gaming giant, says Morningstar.

US private equity firm Blackstone faces more time at the negotiating table and may have to up its bid to ward off any rival suitors, says Morningstar equity analyst Angus Hewitt.

Announced on Monday, Blackstone’s (BX) unsolicited, non-binding offer of $11.85 cash per share values Crown Resorts (ASX: CWN) at about $8 billion. The offer is an 8 per cent premium on Morningstar’s standalone fair value estimate of $11, and a 20 per cent premium on the closing price of 19 March.

Morningstar’s updated fair value estimate of $11.60 incorporates a 25 per cent chance the deal doesn’t go through.

Blackstone, which already owns 9.99 per cent of Crown Resorts, wants regulatory go-ahead for the continuation of Crown’s Sydney gaming licence, as well as a unanimous recommendation from the board.

“This is probably going to be a drawn-out process,” says Hewitt. “Blackstone owned Crown is going to have to prove they’re suitable to operate this licence.

“For shareholders it will come down to price and if it’s a reasonable premium. The takeover premium is quite low. This increases the potential there could be a new offer or new bidder.”

Crown shares closed at $9.86 the Friday before the announcement, valuing Crown at $6.7 billion. By the close on Monday, Crown had risen more than 21 per cent to $11.97.

Crown hit a high of $17.28 in late February 2014.

The board has yet to form a view on the merits of the deal. It was reported on Tuesday that former executive chairman James Packer would support the decision of the board.

Tough year for Crown

Crown Resorts, which is Australia's largest hotel-casino company with more than 5000 electronic gaming machines and 850 tables, has been struggling recently.

Accusations of money laundering and working with organisations involved in organised crime led a judicial inquiry in NSW to find Crown unfit to hold a gaming licence. Inquiries in Western Australia and Melbourne, where Crown also has casinos, are ongoing.

Border and venue closures because of COVID-19 have added to difficulties. Crown posted a $121 million after-tax loss in the first half of fiscal 2021, following net profits after tax of $81.9 million in 2020 and $402.9 million in 2019.

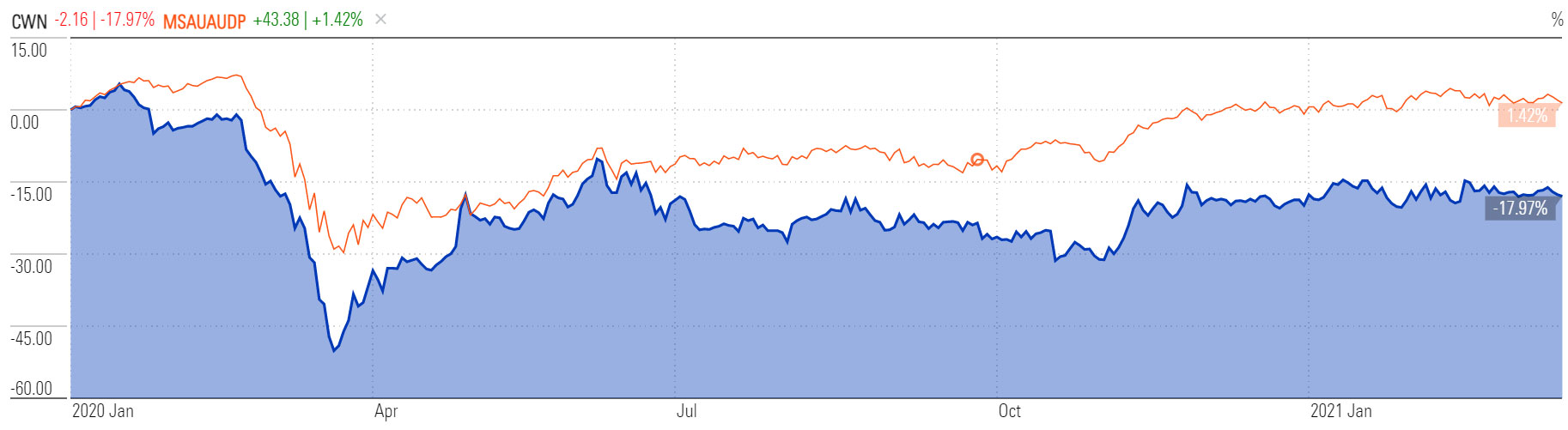

Prior to the offer, Crown’s share price was down 17.96 per cent compared to Jan 2020. Morningstar’s Australia Index was up 1.42 per cent over the same period.

Crown Resorts (CWN), Morningstar Australia PR - 1 Jan 2020 to 19 March 2021

Source: Morningstar Premium

Hurdles to jump

In addition to standard due diligence, the acquisition must get regulatory approval and win over minority shareholders.

Blackstone is no stranger to the casino business. Its involvement with Crown Resorts started last year, when it bought a 9.99 per cent share from Hong Kong gaming tycoon Lawrence Ho’s Melco Resorts. This could help its proposal, Hewitt says.

“Blackstone has industry experience that might help them get this across the line," he says.

"It already owns Las Vegas casino The Cosmopolitan. That would help from a regulator’s perspective. Regulators are probably going to be happy with a proposal which overhauls Crown’s ownership structure.”

Minority shareholders concerned about the low premium—Crown shares traded as high as $12.71 early last year—might hope for new offers or bidders.

Chief investment officer of stockbroker Shaw & Partners, Martin Crabb, said the bid could be a ploy to attract interest from competitor casino operator Star Entertainment (ASX: SGR).

"The question is whether this bid is a ploy by Blackstone about flushing out a competing bid from Star, rather than Blackstone actually wanting to own the assets," he said.

"Blackstone would get a high price for their shares."

Fairly valued Star fell 2.36 per cent on Tuesday to close at $3.90

This is the first takeover offer for Crown since 1 July 1995, according to Morningstar DatAnalysis.