Why investors value dividends so highly

One of Australia's most successful investors and stock pickers explains why a political proposal to tinker with dividend imputation has drawn such passionate responses.

Of late, the headlines on dividends have been primarily focused on the proposed removal of some of the more favourable tax treatments should the Labor Party get elected to power. While franking credits on dividends certainly enhance the attraction of dividends received from Australian companies to many investors, we believe there are many other important reasons why the dividend income earnt from an equity portfolio will always remain an important element to consider when constructing an equity portfolio.

In our opinion, there are three key reasons why dividends have always been and will continue to be an important component for investors to consider:

- Dividends are a more reliable source of return from an Australian equity portfolio

- The level of dividends received is not impacted by the level of the sharemarket

- The dividend yield on stocks can act as a safety net at times of volatility.

Dividends are a more reliable source of return

Over the long term, returns from an equity portfolio come from 2 sources – the capital appreciation from the shares held in the portfolio as well as the dividends received from the shares held.

It is interesting to note that when one analyses the returns from the Australian sharemarket for the ASX 300 of these two components of returns over the last 20 and 40 years the results are as follows:

The importance of the dividend component of an Australian equity portfolio to investors is evident as seen from the table above where almost half of the returns from the Australian sharemarket in the last 20 and 40 years have come from dividends.

The level of dividends received are not impacted by the level of the sharemarket

While the level of capital returns from an equity portfolio over any defined period generally depends on the movement in the sharemarket, the level of dividends received by an investor from an equity portfolio is dependent on the performance of the underlying companies’ earnings, not the movement in share prices.

The level of dividends and the dividend payout ratio of any company is set by the Board of the company and is generally a reflection of the overall profitability of a company and is independent on the level of its share price.

This is an important point to remember as it means that in negative periods in the sharemarket, an investor’s level of dividends from a diversified portfolio – if made up of quality companies with the right attributes – should not vary greatly from year to year and is irrelevant of what is happening on the overall sharemarket.

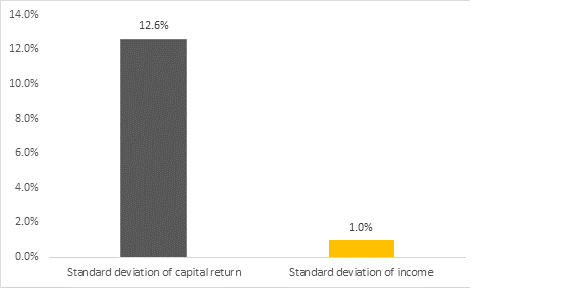

The chart below demonstrates this clearly by comparing the volatility of the level of capital return to the level of dividend from the ASX 300 over the last 20 years.

Chart 1: volatility of returns of capital and income of the ASX 300 over 20 years

Source: S&P ASX300 31/03/1998 – 31/03/2018

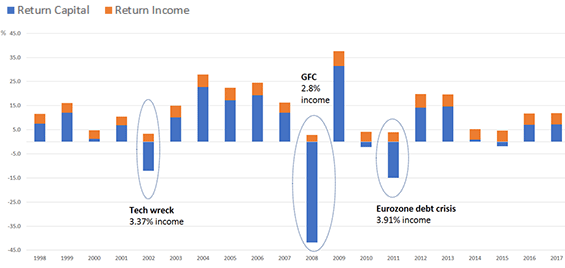

Source: S&P ASX300 31/03/1998 – 31/03/2018This trend is again clearly shown when looking at a breakdown of the level of returns from the ASX 300 in Chart 2 below. One can clearly see that the orange bar- the level of dividends paid from the ASX 300 – has been much less volatile than the level of capital returns (the blue bar) from the ASX 300 over the last 20 years.

Chart 2: Income returns to shareholders from the past 20 years have remained consistent

Source: IML and Morningstar Direct, S&P ASX300 01/01/1998 – 31/12/2017

The key point to remember is that regardless of share price performance, the vast majority of companies in the ASX 300 continue to pay dividends not independent on the mood of the sharemarket which to some extent compensates sharemarket investors for a share price often beholden to the whims of the market.

The dividend yield on stocks can act as a ‘safety net’ at times of volatility

The movement in the sharemarket – particularly over shorter time periods of 6 to 12 months - is more often than not dictated by the mood of investors. In itself, this is impacted by things such as the predictions as to the future level of economic activity, inflation and interest rates, as well as perceptions of geopolitical stability.

Often what are with hindsight quite minor events from an economic standpoint can cause the mood of investors to sour markedly and lead to large declines in the sharemarket. For example, Iraq’s invasion of Kuwait in 1991 led to all sorts of gloomy predictions about an impending global recession by many market analysts and economists.

Times of a perceived crisis can cause many investors to panic, and in such times the prices of most shares can fall heavily initially as many investors/traders often reduce their overall level of sharemarket exposure by rapidly selling many shares indiscriminately and independent of their quality. What I have observed over the many years of investing is that once the panic subsides and some sort of normality is restored, those companies with sustainable earnings that can support a healthy dividend stream are often the shares that can recover the quickest.

The reason for this is fairly obvious – rational long-term investors are always attracted to companies that pay a healthy dividend from a sustainable earnings stream as they understand that the level of returns from dividends is not dependent on future share price performance.

In other words, once shares in quality companies fall to a level where the dividend yield is attractive, this will often attract many long-term investors to buy these shares as they ‘lock in’ often attractive dividend yields, despite a volatile sharemarket.

Conclusion

Dividends provide sharemarket investors with a consistent part of their total return and can also act as a ‘safety net’ in down trending markets.

While we acknowledge that the proposed changes to the tax-effective treatment of dividends in Australia via franking credits is potentially a negative development, dividends will remain an important factor when investing in the sharemarket as they will continue to provide investors with a relatively stable part of returns through the delivery of real cash flow, irrespective of the market cycle.

As a bottom-up value manager, fundamentals are crucial to deciding which companies are included in IML’s portfolios - mainly the quality and transparency of the earnings, cash flow generation, gearing levels or balance sheet strength – which ultimately is what is important in the level of dividends paid by companies.