The turf war for your super: Editor's Note

Amid a wave of mergers, funds have been forced into survival mode.

I've been watching a lot of commercial television recently. I won't say which show; let's just say it's a guilty pleasure. I'm struck by the sheer number of advertisements for superannuation funds. Care Super, Aware Super, UniSuper, Hostplus - they're all there, spruiking their low fees or long-term outperformance. My favourite is the classic Industry Super Australia 'Compare the Pair' ad which spends the whole slot convincing me that I'd always have been better off with an industry super fund before trotting out the line 'past performance is not a reliable indicator of future performance'.

So why now? It's due to a new piece of federal legislation called ‘Your Future Your Super’ or YFYS for short. Either you've heard of it because you're one of the 1 million Australians who received an uncomfortable letter from their MySuper fund disclosing underperformance, or you haven't the foggiest what I’m talking about.

The landmark reforms seek to shake up the industry in several ways:

Duplicate accounts. The legislation aims to weed out so-called zombie accounts by "stapling" employees to one default fund when they start their first job. This hope is to do away with the billions in excess fees and insurance premiums Australians pay every year.

Best interests.It also ups the ante on the fiduciary duty trustees have to members, placing them under a best financial interests duty (BFID) to not engage in any profligate spending that might harm member retirement benefits unduly. Expect spending on football teams, stadiums and news services to come under a harsher spotlight.

Benchmarking. Finally, it sets out a performance test whereby funds will be named and shamed when they underperform APRA-designated benchmarks. Fail once and write to all members telling them the fund has underperformed and they should consider alternatives. Fail twice and you’re barred from accepting new members.

What does this have to do with advertising? The effect of "stapling" members to their existing fund could make it difficult for funds to attract new members, placing greater importance on branding. But more importantly, when the letters go out, there is blood in the water, and the unaffected super funds are in a feeding frenzy to expand membership amid a wave of consolidations.

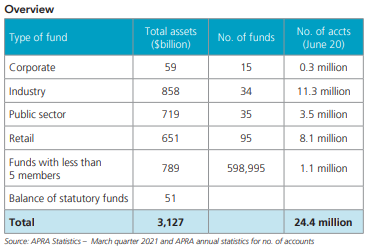

Mergers have been happening for several years among industry funds. VicSuper and First State Super, Equip Super and Catholic Super, MTAA Super, Sunsuper and QSuper and Tasplan (now Spirit Super), to name a few, following pressure from APRA to shape up or ship out. Now, the difficulties of navigating the annual performance test kicks things into the next gear by putting poor performers in the public spotlight and placing downward pressure on fees. Estimates say Australia's superannuation landscape will drop to 12 "mega-funds", each with assets under management of at least $50 billion. According to former superannuation industry consultant Harry Chemay, the game now is to "get big or get out".

But who will stay and who will go? That's up to the members. As funds hit the negotiation tables, the ones with the biggest brands, the biggest membership bases, the best long-term performance and the most funds under management will walk out the victors. As such, the messaging in the ads is clear, simple and one-note. Gone are the days of retirees walking hand-in-hand across a beach or joy riding in classic cars. Today, super is a utility business and two things matter to potential customers - low costs and high performance. With 1 million members in the market for a new fund, the turf war is on for their savings and attention.

Personally, I think member rotation will be slow. In their letters, funds are including explanations for their underperformance which will satisfy most. Many members don't even open their mail. A report in the Sydney Morning Herald this week said a modest number of members in 'dud funds' were heading for the exit. APRA executive board member Margaret Cole points out that any reduction in scale makes it harder for funds to improve their performance. Meanwhile, some of the nation’s largest funds are signing up as many as 1000 new members a day.

As the ad blitz ramps up, APRA is watching. Industry funds are required to act in the best interest of members, which includes their marketing spends. This week, the regulator called out several instances of failure to measure and assess the benefits of marketing spending such as sponsorship deals and advertising spends. While they didn't name names, APRA said one licensee could not demonstrate a link between their spend and any acquisition or retention of members.

“Australians expect those they entrust with growing and protecting their retirement savings to deliver value from every business plan enacted, dollar spent and investment made," Cole says.

******

Rate prediction

Could we see a rate hike next year? AMP Capital seems to think so. In the hours following the release of the quarterly CPI numbers on Wednesday, AMP economists Shane Oliver and Diana Mousina boldly predicted the lift in the core inflation figures could set the conditions for a rate increase by late-2022 as the economy moves into recovery mode. This pushes up against consistent messaging from RBA Governor Philip Lowe that rates are unlikely to rise before 2024, wanting to see inflation sustain within the target range, moving beyond transitory distortions due to the pandemic.

Wednesday's numbers showed an increase in consumer prices of 0.8%, bringing the annualised figure to 3%. However, it was the core inflation numbers that caught people's attention. These figures strip out extreme price rises and falls. For the first time since late-2015, underlying inflation is within the RBA's target 2%-3%, coming in at 2.1%. Back in August, the RBA did not expect core inflation to get above 2% until mid-2023.

In Your Money Weekly, Peter Warnes asks whether housing is the reason why the RBA won't act on inflation.

More from Morningstar

ASIC released its highly anticipated guidance on crypto-asset investment products on Friday afternoon. The publication is a key step in the road to cryptocurrency ETFs in Australia and gives the green light to crypto ETFs directly tracking Bitcoin and Ethereum. Several issuers including VanEck and BetaShares have already expressed interest in listing products. We continue our coverage of cryptocurrency and ETFs this week: Bitcoin ETFs: Should you jump on the bandwagon?; The bull case for Bitcoin; Decoding an ETFs DNA.

In Firstlinks, as house prices continue to skyrocket, Graham Hand considers whether Australia is headed towards intergeneration mortgages, where the house becomes 'ancestral' and is passed with the loan over multigeneration.

Lewis Jackson dives into proposed change to how buy-now-pay-later providers charge fees which could spell lower margins for the major players like Afterpay and Zip.

The UN climate change conference that begins next week in Glasgow, Scotland, is slated to be the most consequential gathering since the 2015 Paris Agreement. What do fund managers want from COP26? Margaret Giles talks to 12 prominent asset managers about what they hope to see.

Finally, I'll be taking a break next week. I leave this Editorial Note in Lewis' very capable hands.

Big bank profit margin tipped to widen alongside higher rates

What rising bond yields mean for the stock market: Charts of the week