The Fed will always rescue the stock market, right? - Firstlinks newsletter

+ Douglass closing interview; Murray's long-term buys; Inflation in commercial property and infrastructure; Family trusts; Aust future; Small cap ideas.

In recent years, investors have relied on the 'Fed put', the belief that if the stockmarket falls, the US Federal Reserve will ease monetary policy and rescue the market. It worked in 2018 when the market fell amid a rate tightening cycle, and the Fed reversed its policies. And of course it happened as COVID struck in March 2020, and central banks around the world rode in on white horses.

Why do we in Australia focus so much on the US? Because it dominates global equity markets, comprising about 56% of total global equity market values, versus the next biggest, Japan at 7%, China at 5% and the UK at 4%. Australia squeezes into the Top 10 at about 2% of global market cap. The US is not only the largest foreign investor in Australia, but the place where Australians invest most overseas.

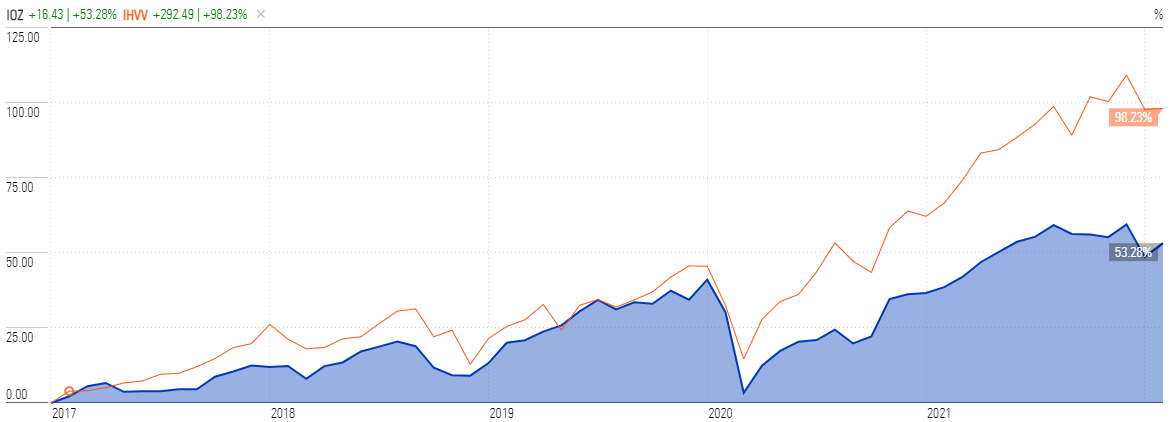

The broad US equity market has performed better than Australia in recent years, mainly due to the success of its tech giants, but the price correlation between the markets is obvious. For example, the chart below shows two index ETFs by the same provider, iShares, with the blue representing the S&P/ASX200 (ASX:IOZ) and the red the S&P500 (ASX:IHVV) over the last five years. If the US market falls in 2022, Australia would surely follow, regardless of conditions in the domestic economy.

Source: Morningstar

It would be dangerous in the current market to assume the 'Fed put' would save investors in 2022. Inflation was recently reported at 7% annual in the US, giving the Fed a bigger problem that it did not face in prior years. It is now committed to tightening and is already considered by most economists to be 'behind the curve' and acting too slowly.

This is one of the many points made by Hamish Douglass in his last interview before taking medical leave as Chairman and CIO of Magellan. The discussion focusses on the way he invests rather than the background relating to his personal life and staff changes at Magellan, which have been covered extensively elsewhere. We also discussed wins and losses in his portfolio and how he reacts to market falls.

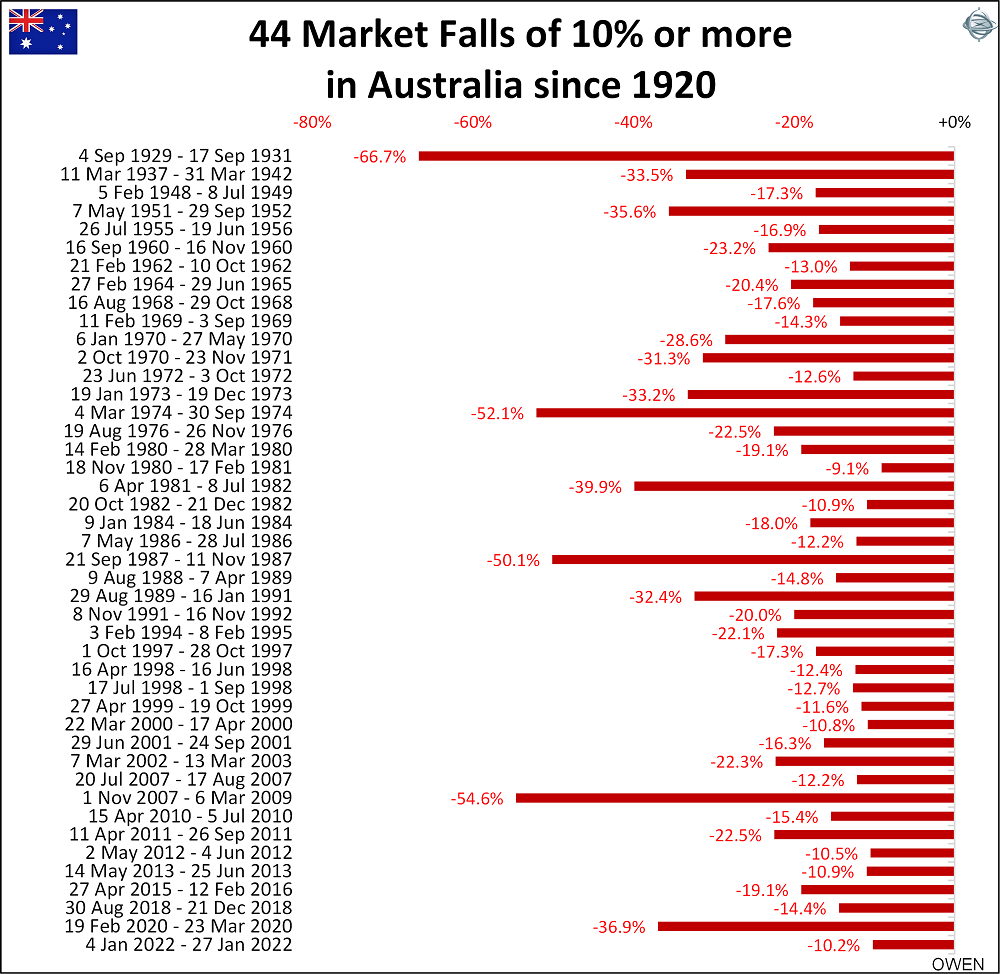

The chart in my article last week surprised some people, judging by the feedback. It is repeated here because it is a vital lesson for all investors. The data shows the reality of sharemarket investing, which every investor should write at the top of their portfolio or screen, and which I repeat regularly at presentations:

Share prices will fall by at least 10% every two or three years, by 20% a couple of times each decade, and by 30% to 50% every generation. Nobody is immune if they hold stocks, so accept it if you want the long-term rewards from equities.

Along the way, there will be winners and losers, but the best approach is not to bet the house but rely on the slow compounding of wealth in quality companies. In the most recent tech fall out, the criticisms of Warren Buffett for his old-world values have reduced as he has caught up with the 2020 and 2021 success of the tech flagship, ARK Innovation Fund.

Before we leave Magellan, here are the latest thoughts of Shaun Ler, the leading Morningstar analyst on the stock:

"Chairman and CIO Hamish Douglass' indefinite leave from narrow-moat Magellan surprised us. But we don't believe this is overly value-destructive for shareholders. In the interim, Chris Mackay and Nikki Thomas will work with Magellan's investment team to manage its flagship Global Equity strategies. The strategies are in good hands. Mackay is Magellan's co-founder, and was its chairman and CIO until 2012. He is currently managing director and portfolio manager of MFF Capital, a listed investment company of Magellan's, whose investment style is parallel to Magellan Global. A Magellan alumni, Thomas was recently portfolio manager at Alphinity, and her tenure saw the Alphinity Global Equity strategy achieve consistent top-quartile performance.

Despite our conviction in Magellan, our concern is not all investors may be willing to ride out this storm. We lower our fair value estimate to $34.50 per share from $38, after factoring in 3% more net outflows than before and further trimming our retail fee forecasts. Douglass' leave could add to the list of reasons for consultants and advisors to consider redeeming or haggle lower fees. This follows Brett Cairn's resignation, news of Douglass' family issues, and concerns of underperformance as its holdings Netflix and Meta de-rated in recent weeks. All are immaterial in isolation, but some could view the culmination of them as a sign of firm instability. Long-time client St James's Place's recent redemption is evidence of this."

In our other profile this week, we also interview Mike Murray of Australian Ethical, who describes why they have launched their first active ETF, a high conviction version of their long-term equity strategy. He also reveals some long-term holdings in companies he especially likes, and a stock he expects to hold for 10 years.

Steve Johnson is a fund manager who looks outside the large companies for the best opportunities, and he thinks small caps are the place where active managers can do best.

Two articles on the impact of inflation of real assets. Steve Bennett and Sasanka Liyanage check how commercial real estate has performed during periods of inflation, while Gerald Stack and Ofer Karliner respond to a reader question on the impact of rising prices on infrastructure assets. They also delve into the relative merits of listed versus unlisted assets in this space.

Family trusts are highly popular investment vehicles for Australians, and Stebin Sam shows how they give tax and ownership advantages while acknowledging they are not for everyone due to a few disadvantages.

And Chris Gibson says the country's future prosperity should not rely on digging up rocks, exporting animals and servicing tourists, but with the right incentives, growth in businesses in technology and health can improve the ongoing chances of success.

This week's White Paper from Fidelity International reports on the retirement intentions of Australians, including the emotional journey, why some prefer to continue working and satisfaction in retirement.

The Comment of the Week comes from Howard Coleman, on the article on risk tolerance and loss aversion:

"Those who more deeply understand the businesses in which they invest, are pleased with the drop in share prices and use this opportunity to add to their positions. Those who have a shallow understanding of the same businesses, worry that 'the market may know something' and are more likely to panic and sell. So loss aversion is heavily dependent on their depth of knowledge of the businesses in which they're invested."