Accessibility is good, but a little bit of friction isn't always a bad thing for investors- Firstlinks newsletter

+ Check your ETFs; Montgomery 2022 stocks; Running the bull; Global leaders on '21 surprises and '22 challenges; Letting debt rip; Gold; ASX IPOs.

One of the benefits of investing in Exchange Traded Funds (ETFs), besides the low fees for the index options, is the ease of entry and exit. Anyone with a broker account needs no fresh paperwork. Contrast this with the pain of many unlisted funds which still require a time-consuming 20-page application process with certified documents, copies of trust deeds, tax and residency checks, identification procedures ... and the name of your dog and favourite colour. Fill in Section A, B, G through K (if applicable). Who can be bothered in a digital age?

However, while 'friction' in business is normally a negative, there are disadvantages in making selling investments so easy when people overtrade. BlackRock CEO Larry Fink tells a story about meeting the manager of one of the world’s largest sovereign wealth funds. The fund’s objectives, Fink was told, were 'generational'. “So how do you measure performance?” Fink asked. “Quarterly,” said the manager.

In her book, “Good Habits, Bad Habits: The Science of Making Positive Changes That Stick”, Wendy Wood, a Professor of Psychology and Business at the University of Southern California, writes:

“Your behaviour is much more controlled by what’s easy in your environment than most of us think ... One of the really nice things about adding friction to a behaviour is that it encourages you to do something else.”

To block bad habits, she says we need to add friction or restraints that turn easy, automatic behaviours into actions that require effort. Some of her tips are to set our phones to light grey to reduce the excitement of checking share prices and overtrading, or removing apps completely. She suggests watching business programmes with the sound off.

Howard Marks says in his latest memo to his clients:

"When you find an investment with the potential to compound over a long period, one of the hardest things is to be patient and maintain your position as long as doing so is warranted based on the prospective return and risk. Investors can easily be moved to sell by news, emotion, the fact that they’ve made a lot of money to date, or the excitement of a new, seemingly more promising idea. When you look at the chart for something that’s gone up and to the right for 20 years, think about all the times a holder would have had to convince himself not to sell."

One way to reduce overtrading is to think about the time and effort involved in investing. It's not only the buy and sell process, but the monitoring, accounting, tax returns and performance measurement. Are you convinced enough about an investment to bother or is it more of a punt? This year, particularly when I'm scaling back exposure to the market, an investment must deserve my attention to warrant the effort. It's counter-intuitive to want more friction but do you spend too much time checking prices and trading for marginal gains?

Although I'm a fan of ETFs for the choice, cost and easy access, there are potential risks in using them that should be considered.

It has been well reported that smaller tech companies without proven revenues are experiencing a sell-off, with 40% of NASDAQ companies off 50% from their yearly highs. At times like this, it is better to focus on resilient balance sheets and companies with pricing power and strong cash flows. While Roger Montgomery is generally optimistic about markets in 2022, he identifies the types of companies that will do better if there is a selloff.

Similarly, Rob Lovelace sees strength in company earnings in 2022. While he expects some level of correction after 11 years of the bull, it's better to weather the storm by staying invested rather than guessing when to buy and sell.

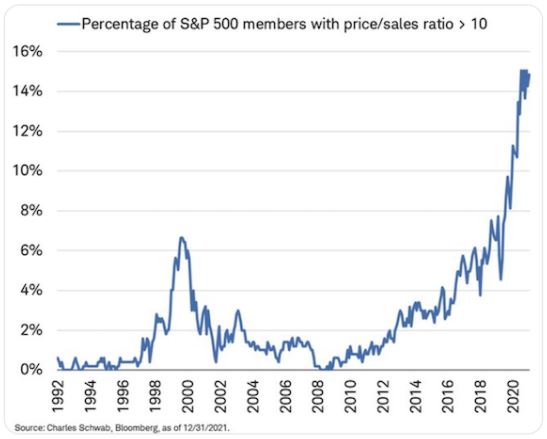

One of the remnants of a rampant bull market and IPOs of companies based on a dream is the move away from judging value based on Price to Earnings (P/E) ratios. It's not possible to calculate a P/E if there's no E, and so promoters of new companies find other metrics, such as Price to Sales (P/S). No longer is an investor deciding whether a P/E of 20 - paying for 20 years of current earnings - is expensive, but a record percentage of companies are trading at a P/S of over 10. No profit so investors are paying for sales.

Still overseas, a friend who writes for the BRINK newsletter sent me a global snapshot of what two dozen of their experts think were the surprises of 2021 and the challenges of 2022, and it's good to read a global perspective at a time of major change.

It's not surprising in such a strong market that 2021 was a record year for IPOs and capital raisings in Australia. James Posnett shows the highlights of 240 new listings, including nine companies with a market cap over $1 billion at listing. While the original owners no doubt did well, not all the new investors have. For example, the largest IPO of the year, fund manager GQG Partners, listed at $2 and is currently $1.82.

Is it time for gold to shine again after a disappointing 2021? Jordan Eliseo looks at gold's potential as inflation and interest rates rise.

And Michael Collins asks the question on many minds: what is the limit to how much governments can borrow? There must be some boundaries or we would not need taxes - governments could simply borrow to meet all expenditures, and promise their populations (and voters!) everything they desire.

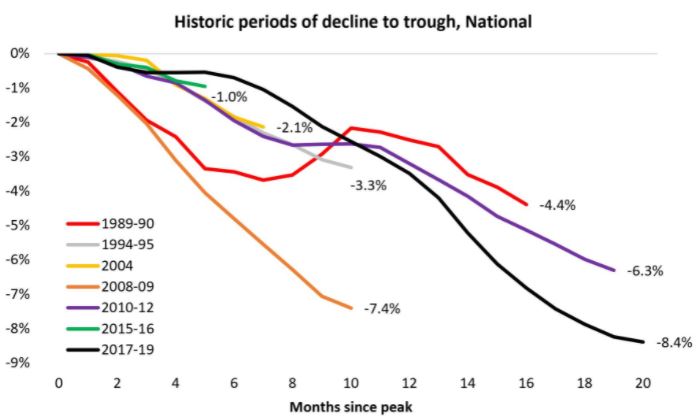

This chart released by CoreLogic during the week brings some perspective to the tearaway national residential price growth seen in 2021. It's tempting to forget that prices do fall. Faced with tight lending conditions imposed by the Financial Services Royal Commission, prices struggled for much of 2017 to 2019. So while 2021 was stellar, there was some making up of lost ground from prior years.

This week's White Paper from Fidelity International looks at the vital subject of demographics. It defines megatrends shaping global growth, and the trends are long term and predictable for investing outcomes.

And it was good to see the Australian Shareholders Association issue a note this week on its top three webinars of 2021.

Look out below for details of the 2022 Morningstar Investment Conference. Filled with star guests, I will be interviewing Hamish Douglass. Due to the virus, the event will be held online, and registration is only $25.