Not all bubbles pop - Firstlinks newsletter

+ RBA switches tack; Bubbles; Super fund letters; EVs 9 companies and 4 minerals; Valuing Tesla; Microsoft multiples; 5 value chains; Super for wealthy.

There is danger in labelling anything a 'bubble', other than if it's a film of soap enclosing air. One person's asset bubble is another's growth story. When Bitcoin went from US$1 in 2011 to US$1,000 in 2017, that was clearly a bubble. It was nearly US$20,000 within a year, another bubble, and peaked over US$60,000 in early 2021. All blowing bubbles. The head of the world's largest bank, JPMorgan Chase CEO Jamie Dimon, told an Institute of International Finance event this week:

“I personally think that Bitcoin is worthless. Our clients are adults. They disagree. If they want to have access to buy or sell Bitcoin – we can't custody it – but we can give them legitimate, as clean as possible, access. No matter what anyone thinks about it, government is going to regulate it. They are going to regulate it for [anti-money laundering] purposes, for [Bank Secrecy Act] purposes, for tax."

Hamish Douglass wrote the same in this Firstlinks' article. Many comments claimed Hamish simply did not understand. Bitcoin has been written off all along and I have no idea where it is going.

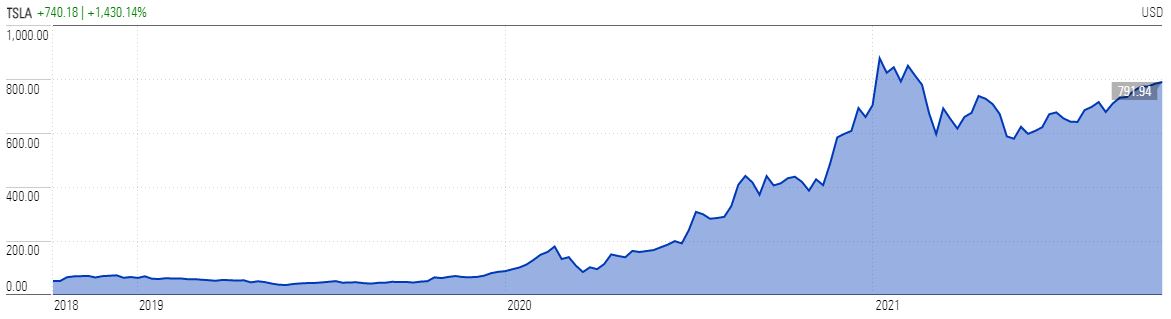

Same with Tesla. The Morningstar chart below of its share price shows how the true believers have been rewarded. As every major car manufacturer rolls out its electric vehicles and others select hydrogen, some analysts say it's already in a bubble around US$800, while others say it's worth US$3,000.

And so to Australian house prices. It's the Great Australian Dream and panic, FOMO, supply shortage and low rates continue to drive gains at these heady levels. How can a house price be in a bubble if someone lives in a lovely home for 30 years? There is a real estate agent who specialises in an inner west Sydney suburb who hands out a promotional brochure saying he has been selling houses and living there for 20 years. It says he was the first agent to sell a house in the suburb for over $1 million. Must have seemed like a lot for the inner city, $1 million. His brochure says he was first over $2 million. $2 million! And $3 million, and $4 million, and $5 million and $6 million. He just reprinted his brochure to acknowledge the first sale over $7 million, to a local family upsizing. No waterfront, busy street, sloping block.

Gareth Aird and Kristina Clifton report on how the Reserve Bank is leaving it to APRA to control house prices, but with a remarkable quote from a previous Governor, Glenn Stevens. In 2014, Stevens said the central bank would be 'unwise' to put unemployment above controlling house prices. Now the bank has done a backflip, although they do admit in their latest Financial Stability Review:

“Price falls could be widespread if interest rates were to increase sharply due to unexpected inflation or rising risk premiums. Sharp price falls could cause greatest harm to the financial system for assets where leverage is common, notably residential and commercial property.”

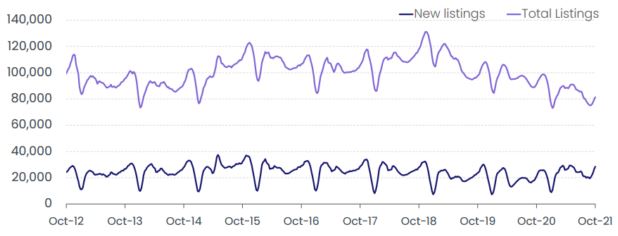

The CoreLogic table on listings shown below is finally showing an uptick in supply which might help take the edge of further price rises.

The first announcement by APRA last week was strange because it said a research paper on possible prudential changes would be ready within two months, but then within a week, the first tightening (on the rate 'buffer' calculation) was introduced. Someone gave them a nudge, and more new rules are coming. As Wayne Byers, Chairman of APRA, said last week:

“While the banking system is well capitalised and lending standards overall have held up, increases in the share of heavily indebted borrowers, and leverage in the household sector more broadly, mean that medium-term risks to financial stability are building.”

The inflation drums also grow louder every day, and many central banks are considering their monetary policy settings. Yesterday at a Citi Investment Conference, former US Treasury Secretary Larry Summers said the US economy is overheating and a shortage of Labor is another factor pushing up prices, and he criticised the Federal Reserve’s lack of action as inflation surges.

It will make Governor Philip Lowe's argument about no rate rises until 2024 harder to sustain. This week, the International Monetary Fund said the global economy is entering a phase of inflationary risk, and it called on central banks to be “very, very vigilant” and take early action to tighten monetary policy if price pressures continue. As we have discussed before, household debts are too high to withstand rate increases but inflation needs to be controlled.

We have two articles on the bubble theme. Amit Nath explains why so many people miss out on the great growth stories such as Microsoft and Amazon until it is too late. There is a misunderstood focus on current earnings and a human inability to understand exponential growth. Are we hard-wired for failure?

Which takes us back to Tesla, and a lively debate summarised by Emma Rapaport between the world's highest-profile Tesla bull, Cathie Wood, and fundamental value investor, Rob Arnott. They both make convincing cases, and we can look back in five years and wag a finger at one of them. We also attach an edited transcript of this fascinating look at both sides.

Dawn Kanelleas describes the impact of electric vehicles on the demand for batteries, and she identifies four key commodities and nine Australian companies likely to benefit. While there has been a lot of attention on hydrogen recently, it's hard to ignore the move to electric cars. In Norway, they expect no more petrol or diesel cars to be sold there by early next year.

We have described in detail the problems with ASIC's performance test for some large funds (such as here and here), but the fund letters have now gone to members. We check how super funds which failed the test under the Your Future, Your Super legislation are communicating. A modified version of the 'Contrast Principle' is getting a good workover.

Every company must adapt to change, especially with digital disruption, and Hendrik-Jan Boer gives five value chains that 'transition winners' are adopting. Every company needs to adopt one or more of these chains.

Professor Kevin Davis was a member of David Murray's Financial System Inquiry a few years ago, and he has taken a swipe at the Government for allowing retirees with super pensions to draw only half the amount required under the normal rules. Anyone planning their cashflow for next year should not expect this favour which allowed wealthy people to leave even more in a tax-advantaged structure.

A shout out to the 2021 Sohn Hearts & Minds Conference (where the co-founder of Firstlinks, Chris Cuffe, is Chairman of Hearts & Minds Investments (ASX:HM1) which will be held on 3 December 2021, with a stunning headliner in Charlie Munger. Tickets and details at sohnheartsandminds.com.au. Chris tells me if people want to hear Munger they must buy a ticket for this charitable cause as the event will not be recorded.

This week's White Paper is a further development of the Neuberger Berman piece on value chains, identifying transition winners that are durable, sustainable and adaptable.

And our Comment of the Week is from Tony on Ashley Owen's article on property prices (which has already received almost 30,000 views):

"Your analysis leads me to believe that we are in for a significant correction, or even crash, in property prices as soon as interest rates rise. People with mortgages borrowed like drunken sailors, both first timers and “investors”, in the belief that property has never fallen in value. They overlook the fact that the current mix of events (zero interest rates, massive mortgages, zero pay rises), never happened before. The confluence of these three events means we are heading for the rocks when it comes to property values. The fallout will not pretty and everyone, the RBA, APRA, the Federal Government, the Opposition, will always be pointing fingers at each other for the blame."