House prices still mostly an owner-occupier affair

Despite a big jump in investor lending, credit to investors remains low by historic standards and headwinds persist, says the RBA.

A “flood”, a “rush”, a “surge”. That’s how the press has depicted the re-entry of investors into the housing market.

The figure that launched a thousand ships was 12.7 per cent. That’s how much lending to investors grew in March: $7.8 billion, according to ABS data released on Wednesday. The figures are a 54.3 per cent increase on March 2020. Over the same February to March period, loans to owner occupiers only rose 3.3 per cent to $22.4 billion.

But the RBA isn’t joining the clamour over investors, choosing to keep the limelight mostly on owner-occupiers in its May “Statement on Monetary Policy”.

“Housing credit growth has picked up, with strong demand from owner-occupiers, especially first-home buyers,” the central bank said in Friday’s report.

“Investor credit has also been growing, but at a slower pace than credit to owner-occupiers; conditions in rental markets have been quite uneven, which has been weighing on investor demand for properties in some markets.”

The RBA put the recent growth of investor lending in historical context, while emphasising the headwinds that remain for investor activity.

“Investor credit growth remains low by historic standards and there are a number of factors that may weigh on investor activity in the period ahead, including lower rental yields, high vacancy rates in some areas and lower immigration.”

Border closures sent vacancy rates soaring and rents tumbling for inner-city apartments in Melbourne and Sydney, often favoured by investors. Price growth for apartments has lagged houses in recent months. In April, units in Sydney and Melbourne grew, respectively, 1.3 per cent and 1.0 per cent, according to CoreLogic. Meanwhile, houses in Sydney rose 2.8 per cent. Melbourne clocked in 1.4 per cent.

David Bassanese, chief economist at ETF provider BetaShares, agrees about the headwinds, but thinks this could force capital city investors to seek bargains in the suburbs.

“The headwinds are true for apartments, but less so for stand-alone homes. To the degree investors come back they may compete for detached homes in capital cities,” Bassanese says.

“It has to get a lot hotter before the RBA will act, but I think it will.

“My base case is macroprudential controls will come in later this year. Who they target and if it will specifically be investors depends on how things evolve.”

Regulators watch the behaviour of investors and owner-occupiers closely. In 2017, the banking regulator APRA set new lending rules targeting investors and interest-only loans to tamp down house prices.

But in recent comments, APRA chairman Wayne Byres said he was unconcerned about rising house prices as long as lending standards stay tight. So far, he thinks banks have done a good job on this front.

“Risk for the financial system occurs when lending standards are poor or weak,” he said during a Committee for the Economic Development of Australia event last Wednesday.

“We don’t see that up to now – banks have done a pretty good job in holding lending standards up.”

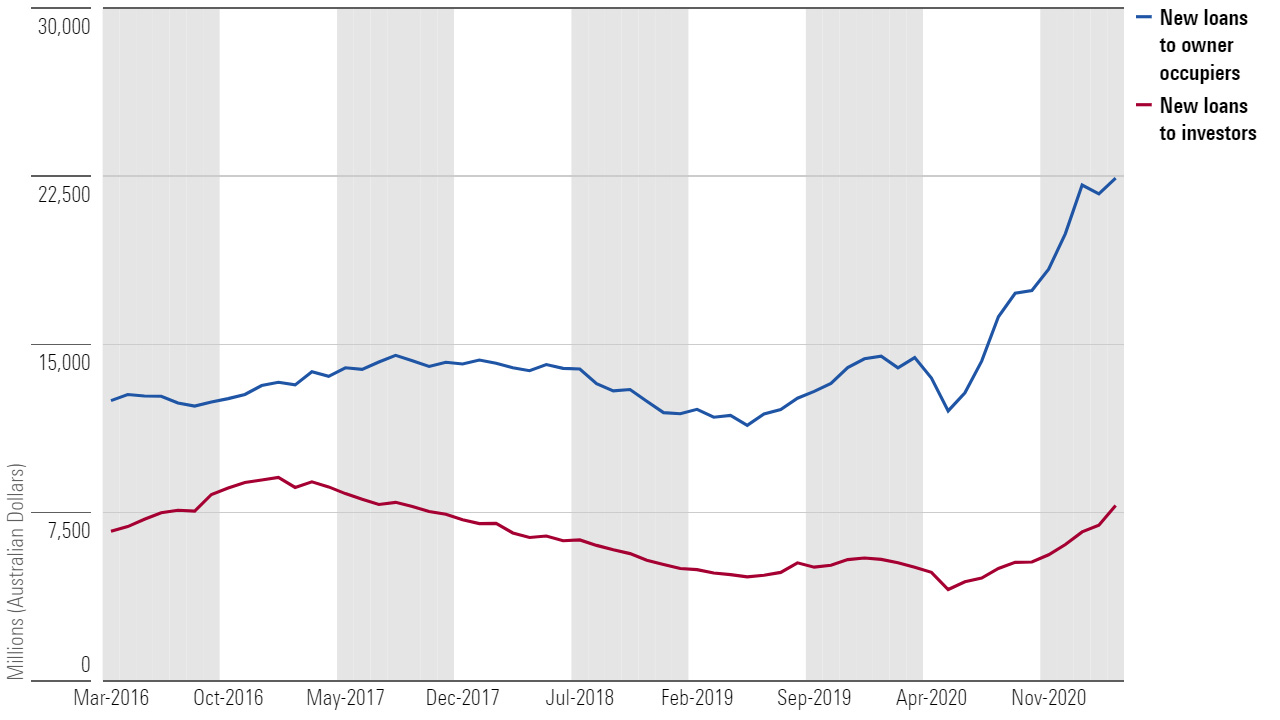

Investor lending recovering from a deep trough

This week’s figures from the ABS are a rebound from a low base. Between March 2017 and January 2020, the monthly flow of loans to investors – new loans being written – fell by 39 per cent. Flows hit a low last May, from when they have risen steadily. But the growth has considerably trailed new loans to owner-occupiers.

New loans for property (March 2016 - March 2021)

Source: Australian Bureau of Statistics

New loans to owner-occupiers in March were about four times the size of those going to investors: $22.4 billion to $7.8 billion. That dollar figure gap between owner-occupiers and investors has widened steadily since late 2016. The gap closed very slightly in the March quarter but is still barely off record highs.

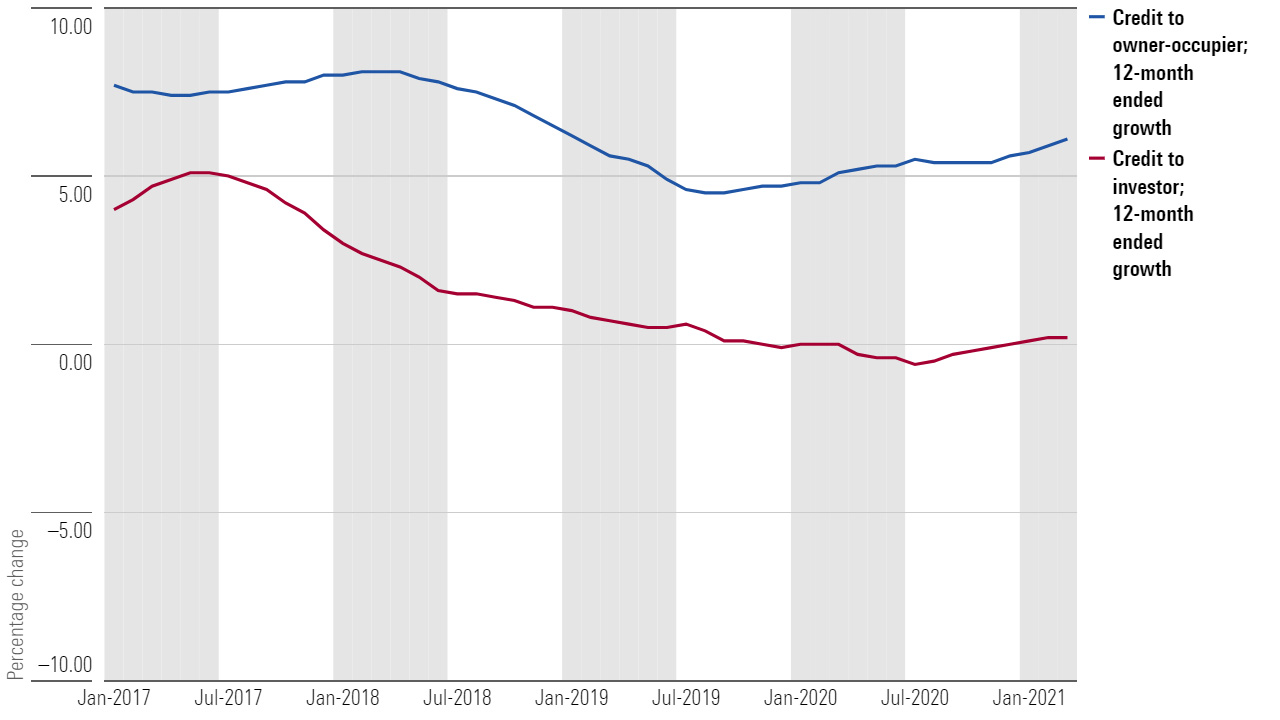

The RBA’s figures for March show credit growth to investors held steady at 0.2 per cent, the same as February. Owner-occupiers rose by 6.1 per cent. The RBA’s figure for investors is considerably smaller than the ABS’ because the ABS just measures new loans made, while the RBA measures changes in the total value of outstanding loans. The $7.8 billion in new loans measured by the ABS are less than 1 per cent of the $670 billion in loans outstanding.

Growth in credit to residential property (Jan 2017 - March 2021)

Source: Australian Bureau of Statistics

For Bassanese, the RBA’s attitude to the housing market represents a shift in their thinking on asset prices - a potentially complacent one.

“We’ve swung 180 degrees on real estate. Regulators used to be more concerned about asset prices.”

“Deputy Governor Guy Debelle recently called asset prices part of the monetary policy transmission mechanism. It’s a shift in thinking to greater complacency.”