Firstlinks newsletter - 28 January

Loving stock stories and funds; Buffett win and lose; themes for 2021; investors Breaking Bad; retiree SG increases; buying banks; home affordability.

When we wrote about Robinhood and Reddit investors in June last year, it was not expected that their activities would ramp up to another extreme level. Fuelled by stimulus cheques and social media stories of instant wealth, thousands of new participants in the US are speculating in a way the market rarely sees. Think Dutch tulips in 1637, South Sea Bubble in 1711, the Japanese stock market in the 1980s, Alan Greenspan's 'irrational exuberance' of 1996, the dot coms of 2000 and US housing before the GFC.

When a stock like GameStop rises 125% in five days, 300% in a month and 1,900% in six months, and it's a video game retailer with declining sales, speculators have no regard for the underlying business. It is already a case study in the power of unified individual investors. Thousands of people are joining Reddit groups, deciding to buy a stock and take on the professional hedge fund shorts, who are then forced to buy to cover their positions. There are also losers as GameStop fell 60% in an hour before resuming its rise. The US market has never seen options and retail activity at this level before.

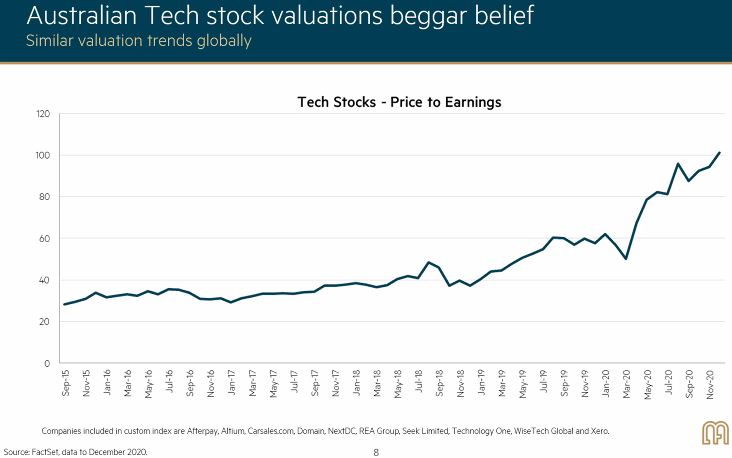

Obviously, this is not on the same scale as Australian tech winners such as Afterpay, Xero, WiseTech and Altium, which are real businesses with share prices riding a wave of optimism. But they are causing a performance problem for some of our more respected fund managers who use fundamental analysis. They can't match the growth market rise and are forced to explain their 'underperformance' to their clients. A fund manager with a long history such as Maple-Brown Abbott is using the following chart, among others, to show how a custom index of Australian tech stocks has reached a Price/Earnings ratio over 100 which 'beggars belief'. These managers will benefit when the market finally rotates from growth to value.

This week, we look at the difficulty facing investors who attend fund manager presentations for insights into the quality of the manager. Performance is in the past and there is no way of knowing whether the manager will deliver in future. In addition, every presentation makes a good case for support leaving investors with unlimited choices.

Kate Howitt describes the investor dilemma of deciding whether to participate at elevated prices in the risky game of speculation as a 'Breaking Bad' moment. Spoiler alert, that does not end well for the main character but financial markets are not at that point.

Nobody could accuse Warren Buffett of taking a short-term, speculative view on the market, but even he and Charlie Munger went into their first IPO for years by investing in Snowflake. And they have a big position in Apple. James Gard look at Buffett's portfolio in 2020, where not everything went as well as the tech exposures.

Olivia Engel sees a return to some normality in 2021, where a company's share price better reflects its business fortunes, and she identifies the sectors and themes she expects to pay off. Likewise, the renewed optimism that our major banks have withstood the worst of the pandemic is reflected in recent price rises, and KPMG runs its ruler over the resilience of bank balance sheets.

During the pandemic, while some people enjoyed business and market success, many others have struggled. One way to stimulate the economy is through more social housing, and Matthew Tominc suggests ways this can be done while still meeting the reasonable investment return needs of savers.

The Minister for Superannuation, Financial Services and the Digital Economy, Senator Jane Hume, turned up the temperature in the super debate with a piece in The Australian Financial Review on 22 January 2021. It started with a strange comparison between retirement savings and a bikini:

"We all tend to make the most of our best assets ... If you have a fabulous bikini body, surprise, surprise, you tend to wear bikinis. It’s human nature to make the most of what we’ve got. Except, strangely, when it comes to our retirement savings."

Anyway, she highlighted that many retirees live unnecessarily frugal lives and die with most of their savings intact. The challenge for policymakers is:

" ... how to improve the confidence of retirees to use their savings more efficiently to enjoy a better standard of living."

It's a debateable definition of efficiency, with Senator Hume promoting the availability of reverse mortgages and the age pension to cover a loss in savings.

"For example, as superannuation balances decline over time the social security safety net available to all Australians will kick in, providing a part pension that scales up as superannuation balances are drawn down."

I'm guessing most readers of Firstlinks do not plan to draw on an age pension, but future increases in Superannuation Guarantee are clearly in jeopardy. Roger Cohen offers his view on whether this is the correct policy.

With the recent rise in the CPI, the ATO has announced the first increase in the Transfer Balance Cap (TBC) from $1.6 million to $1.7 million from 1 July 2021. Only people who start a pension after that date will be eligible for the higher cap. Super is already complicated enough and soon we will have TBC amounts specific to particular people.

This week's White Paper from Franklin Templeton looks at a product that is at the centre of a battle between improving standards of living and decarbonising national economies.