Are interest rates heading negative Down Under?

There is a chance that negative interest rates could hit Australia in the near future, according to several global fund managers.

There is a chance that negative interest rates could hit Australia in the near future, according to several global fund managers.

Even the Reserve Bank of Australia governor Philip Lowe recently told the standing economic committee he couldn't rule out the unconventional step of forcing the cash rate into negative territory.

The cash rate stands at a record low of 1 per cent. A negative rate would aim to stimulate the economy further by encouraging people to borrow and spend rather than save.

Good for the economy perhaps, but less so for investors chasing yield and income.

In a global market environment where the US 10-year bond yield has fallen below its 2-year equivalent for the first time in 12 years - and Australia's 10-year yield last week dipped to a historical low - it seems almost nothing is off the table.

Part of this mix is the continuing US-China trade uncertainty and tit-for-tat pronouncements from Presidents Donald Trump and Xi Jinping.

"What's going on in China, what's going on in the US, all of that uncertainty and the pivot we've seen in the Fed and the RBA cutting rates...that's all connected with then just saying the global pieces are really coming together.

"And as much as we'd really like to look at the Australian economy by itself, we're a really small open economy, and what happens in China and in the US is still really important," said Michael McCorry, chief investment officer, BlackRock Australia in a Sydney briefing this week.

"Watching these two big superpowers duke it out over trade, it does have implications for us as well, and for the correlation of bonds and equities in investment portfolios."

Insatiable hunger for yield

The risks for investors who are approaching retirement and hunting for yield have been highlighted by several asset managers in recent days.

The share market downturn is fuelling what Clime Asset's Adrian Ezquerro describes as "an insatiable appetite for high-yielding assets" on the part of investors.

Charlie Lanchester, who heads up BlackRock's concentrated industrial share fund, says he can see retirees being forced further into risk assets. "So you've got to be very careful in how you invest,” he says.

McCorry too shares these concerns. "There's a lot of risk around now, but through an income generation lens,” he says. “The Australian equity market is throwing off a little over 5 per cent dividend yield, you get franking credits on that, it's probably a nice yield for retirees, but there's a lot risk around that."

Earlier in the week, Fidelity portfolio manager, Kate Howitt, said the lack of yield from sovereign bonds or term deposits is prompting retirees to consider equities, listed property and alternative assets.

"All of this stuff that really is quite risky and scary and can be high volatility," Howitt said.

Rates could head into red

Considering whether rates in Australia may soon dip into the red – as they have in Switzerland, the Euro zone and Japan - McCorry says he wouldn't have considered it a possibility 12 or even six months ago.

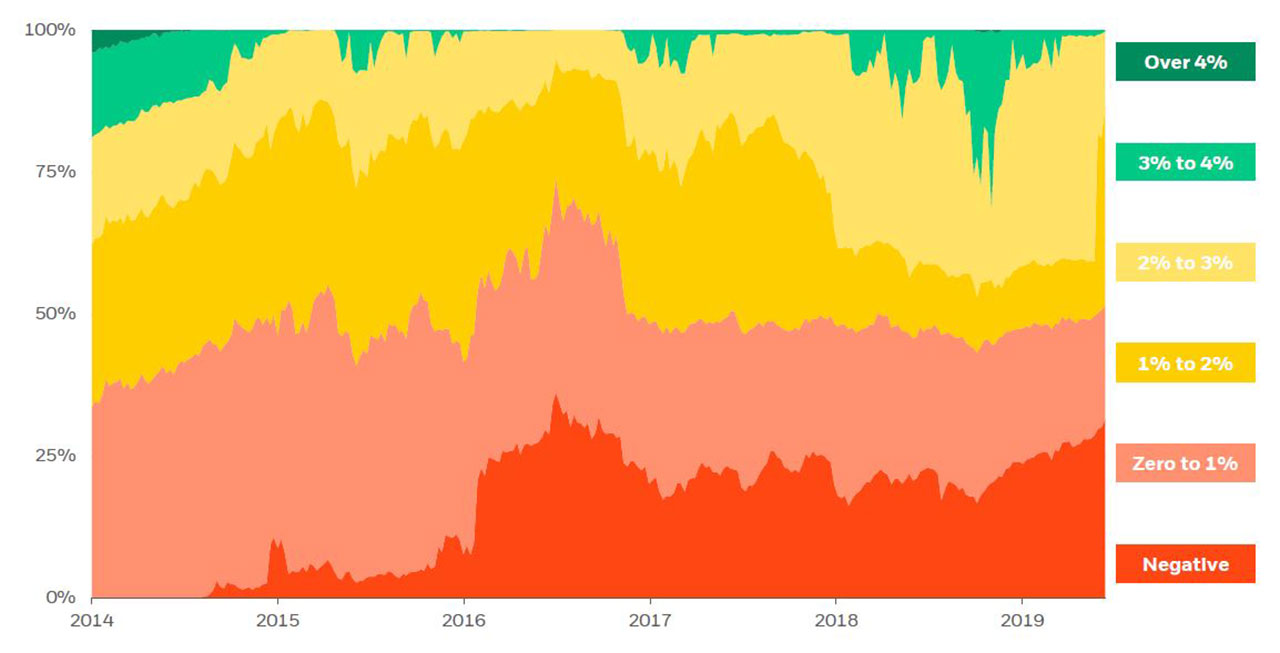

The universe of bonds with negative yields is growing

BlackRock Investment Institute, with data from J.P. Morgan and RefinitivDatastream, July 2019. Notes: The chart areas show the share of bonds by market value within the J.P. Morgan Global Developed Bond Index with yields in each range.

"But now I would say it's not outside the realms of possibility, though it's certainly not our base case," says McCorry.

"It could happen, but I come back to the point that we believe the Australian economy is in good shape, and we don’t see it slipping into recession."

Yesterday's ABS announcement of steady employment levels for July is one example referenced by various commentators, including RBA deputy governor Guy Debelle.

He suggests the decline in house prices, which has been a major drag on Australian consumption growth, may also be at an end.

"If this is the case, the drag from declining wealth and turnover will dissipate. Housing market conditions may even start to support consumption growth again in the period ahead," Debelle said in a speech at the annual Risk Australia Conference in Sydney on Thursday.

Vanguard Australia's head of fixed income, Jeff Johnson, voices a similar but more upbeat assessment to that of BlackRock's McCorry.

"I don't think anyone can rule out negative rates, but we are a fair distance away from that here in Australia.

"The RBA is still at 1 per cent, so there is ample room for them to ease further, should conditions further deteriorate," Johnson says.

He suggests that negative interest rates wouldn't have been on the radar of many investors until recently, "but of course, it's been a phenomenon that we've observed in Europe to some degree and also in Japan.

"But now what we're seeing is a bit of weakness globally - investors are becoming more concerned about a potential recession.

In the US, Inflation remained around 2 per cent year-on-year in July – in line with the Fed's preferred level of around 1.6 per cent.

In Australia, the RBA's underlying inflation forecast was 1.5 per cent for August – it was looking for 2.25 per cent last November.

"Inflation has remained relatively dormant globally, despite reasonably healthy labour markets and you add to all of that certainly an increase in geopolitical risk, and you know, it's not a surprise that we've seen interest rate markets reprice, with yields falling," Johnson says.

What should investors do?

As we've seen, a flow-on effect of rising volatility and the wild ride of equity markets in recent days and weeks can prompt investors - particularly those relying on bond or equities for income, such as retirees - to make rash decisions.

But Morningstar's director of investor education Karen Wallace casts doubt on the widely held idea that the inverted yield curve is a precursor to a recession.

"To say that an inverted yield curve signals an economic slowdown is imminent is an oversimplification,” Wallace says.

“But it does point to a risk in our current financial system: A flatter yield curve can hurt lenders' profits and stability and their willingness to lend.”

An inverted yield curve occurs when the interest rates on short-term bonds are higher than the interest rates paid by long-term bonds. In short, investors fear what the short-term holds and instead opt for longer-term bets.

"If long-term and short-term rates are close, markets must be expecting little growth or lenders would demand a bigger time premium, Wallace says.

"At Morningstar, we don't recommend that investors retool their portfolios just because the yield curve is not following its normal path. That said, it's not a bad idea to check in on whether your portfolio is well positioned to weather a rough patch.”

Wallace cites Christine Benz's “Bucket portfolios” as a useful investment strategy for times such as this. This concept holds that assets needed to fund near-term living expenses ought to remain in cash and other safe, liquid short-term assets.

"Money that you won't need for several years or more, meanwhile, can be invested in a diversified pool of long-term investments such as equities,” Benz says, “with the cash buffer providing the peace of mind to ride out periodic downturns in the longer-term portfolio."