Lessons from running a fund for 10 years

Andrew Mitchell of Ophir Asset Management on the key rules of investing, some of the fund’s winners and losers, and where he's finding value now.

Ophir Asset Management’s Opportunities Fund recently celebrated its 10-year anniversary. It’s been a stellar performer, returning more than 21% net of fees since inception. Ophir Co-founder Andrew Mitchell tells Morningstar’s Wealth of Experience podcast that the main lesson he’s learned from running the Opportunities Fund is that markets are volatile, and they tend to reward those who stay consistent with their investing over the long term:

“… it's really just staying the course as an investor, sticking to your process, and not getting worried out of positions that you believe in. Likewise, I guess investors listening here, not getting worried out of the market because capitalism works. It runs and it keeps winning.”

Mitchell thinks it’s important to set realistic expectations for investors. He tells prospective and current investors that the fund hasn’t gone up in a straight line, even though the long-term returns have been healthy.

Volatility is the price of admission

He recalls working at a previous fund which fell around 50% during the GFC, underperforming the market at that time. That fund bounced back in a big way, though he likes to show investors that falls like that can happen and they need to prepare for that. And if they don’t hold on during those tough times, they’ll probably miss the sharp rebound that usually happen after a large dip.

Mitchell says it’s no coincidence that when his fund performs well that the phone rings off the hook, rather than the other way around.

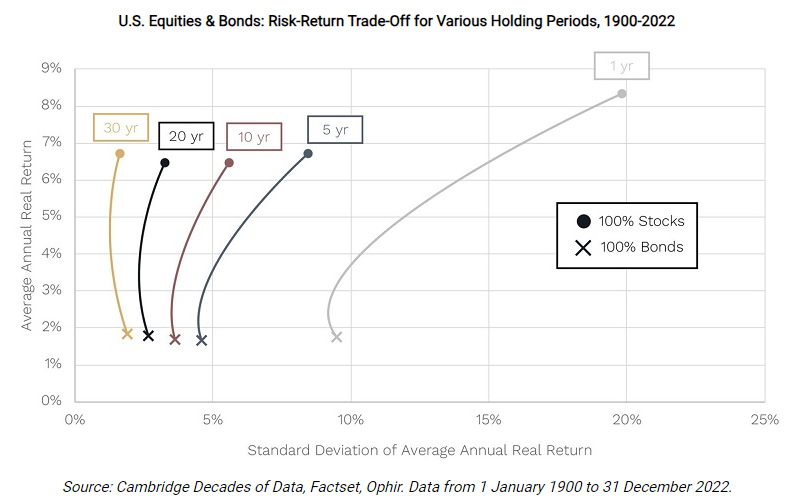

In the podcast, Mitchell outlines why he’s a big believer in equities as an investment class. Earlier this year, he wrote an article for the Firstlinks newsletter with the provocative title, ‘Stocks are less risky than bonds in the long term’. In it, Mitchell suggests that on a one-year timeframe, equities are far riskier than bonds. Yet, the longer your timeframe, the less risky stocks become. He says on a 20-year timeframe, stocks are about as equally risky as bonds, and over 30 years, they’re less risky.

As for how the macroeconomic environment fits into his strategy, Mitchell says that if you’re not thinking about it, “it's like trying to swim with an arm behind your back. You're not going to be too successful.” He says that while the fund focuses on bottom-up investing, the macro can drive the earnings of companies. Ultimately, his goal is to work out something about a company that the market hasn’t and that can drive long-term value.

Big winners

Mitchell’s fund is most famous for investing in Afterpay just after it IPO’ed. And it held onto the position to make many multiples of its money. Mitchell emphasizes that he did a lot of work to understand the company early on. He talked with unlisted retailers who were telling him that Afterpay was driving their online sales, customers loved it, and it was changing their spending behvaviour.

He invested in the stock thinking that making 2-3x his money would be a good outcome. Never did he expect it to go up 50x. They key in his eyes was not selling out as the share price rose. Yes, his fund did cut their holding as the price spiked, yet it held on to most of its shares because it believed in its original thesis for owning the company.

As for current stocks that he thinks may become big winners, Mitchell points to a US small cap stock called TransMedics Group (NASDAQ: TMDX). This company is involved in the removal, storage and transportation of hearts, lungs and livers used for organs. Their technology enables them to keep the heart beating outside of a human body.

Mitchell says TransMedics is growing the number of organ transplants that happen in the U.S. From 2005 to 2020, the amount of heart, lung, liver transplants went from 10,000 to 15,000. In the last three years, it's gone from 15,000 to probably 19,000 this year. In other words, the size of the market is expanding rapidly partly because the company makes doctors’ lives easier.

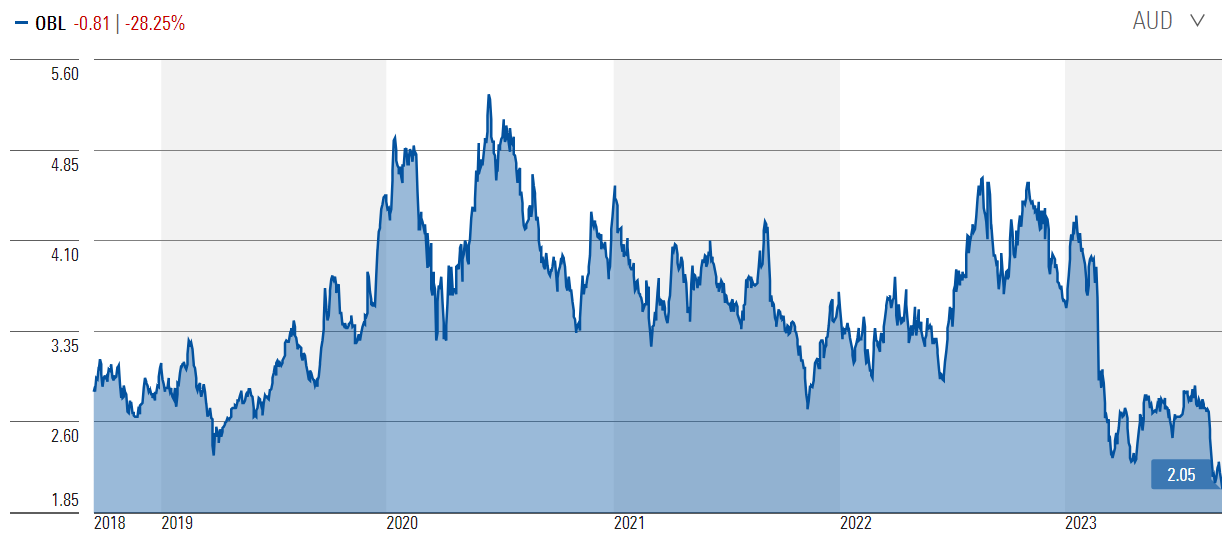

A loser, for now

A stock that hasn’t been working for the fund is ASX small cap, Omni Bridgeway (ASX: OBL). This company provides funding for litigation. Given unpredictable timeframes for the completion of court cases, it makes for considerable earnings volatility from year-to-year, something investors often don’t appreciate.

It’s not a large position for Mitchell, though it’s been a painful one so far.

The opportunity in small caps

Mitchell says the theme that is dominating his thinking right now is the bear market in small caps and, conversely, the opportunity that brings. He says everyone is focused on the performance of large cap technology stocks, especially the ‘magnificent seven’ (Tesla, Microsoft, Alphabet, Nvidia, Apple, Meta, and Amazon) that have driven the S&P 500 this year. Yet, small caps have been left behind:

“… the market will come back for them at some point and there will be a lot of money to be made. It's not a matter of if, it's just when, and we don't know the when part. But this will be a time that we'll all look back at and say this was a great opportunity. I'm not sure whether you could say that about the Magnificent Seven, and I'm not all over NVIDIA. It's obviously a fantastic business, it just trades at, I think, 25 times plus forward revenue.”

You can listen to the full interview on the Wealth of Experience podcast here.

James Gruber is an assistant editor at Firstlinks and Morningstar.com.au