ESG investments improve performance; or do they?

The rapid growth of ESG investment options in recent years has increased the burden for fund selectors and investors who want to build ESG portfolios.

Mentioned: Candriam Sustainable Global Equity (12328), Acadian Global Equity (12403), Generation Global Share (15813), Pengana WHEB Sustainable Impact (15887), Bell Global Equities Wholesale (16705), Schroder Global Sustainable Equity - WC (17701), Pengana Axiom International (3876), CFS FC WS Inv-Capital Group New Persp (40543), AXA IM Sustainable Equity (40549), Australian Ethical Intl Shr WS (40968), Dimensional Glb Sstnblty Trust Unhdg (41064)

The rapid rise in environmental, social, and governance-themed funds is among the industry’s fastest-growing trends. Whether in a managed fund, exchange-traded fund, or superannuation form, ESG investing seems to have captured the imagination of investors in a way that most other forms of active management have struggled to do for many years.

A flood of new ESG strategies have subsequently launched in Australia to try to benefit from this trend, as asset managers look for ways to achieve growth in a world where passive funds and a seemingly never-ending downward squeeze on fees have challenged existing asset-management business models. But why is this growth in demand for ESG investments occurring? Do ESG funds achieve better performance than comparable non-ESG funds? Do ESG funds reduce risk relative to comparable non-ESG funds? Or is this simply investors using their money as a means of personal-values alignment, regardless of risk-adjusted performance outcomes?

This article explores these issues in detail through the lens of the Australian investable ESG opportunity set, drawing some important conclusions for constructing ESG portfolios.

The rise of ESG investing

The most significant structural growth trend over the last decade in asset management has been the rise of passive or index-tracking investments, as investors have increasingly looked to reduce the costs of their portfolios in an environment where active managers have, on average, struggled to deliver in many sectors. But a new structural growth trend has emerged: ESG investing.

ESG investments have been around for a long time, but in Australia they have only achieved small incremental growth off a small base for many years. But in the last couple of years that growth has taken off, not only in Australia but around the world. The Australian bushfires in late 2019 certainly put ESG investing in the limelight as the effects of climate change came to the forefront globally.

This growth was quickly turbocharged by the onset of the coronavirus pandemic in 2020, a pattern that has continued into 2021. According to Morningstar’s Sustainable Investing Landscape for Australian Fund Investors report for Q2 2021, assets in Australian Sustainable Investments were AUD 33.42 billion on 30 June 2021, a 66% increase from a year earlier. Asset managers have seen this trend and launched ESG funds in an attempt to capture some of the action.

Exhibit 1 shows the launch of Australian-domiciled ESG funds over time, with growth in new products taking off since 2016, while Exhibit 2 shows that assets began to increase in early 2020.

Exhibit 1: Australasia-domiciled sustainable fund and ETF launches

Source: Morningstar Direct. Data as of 30 June 2021

Exhibit 2: Estimated net flows of Australasian sustainable investments (AUD, Mil)

Source: Morningstar Direct. Data as of 30 June 2021. Excludes funds of funds

Have ESG funds delivered better outcomes for investors?

At Morningstar, we always encourage investors to make decisions for the long term, and our analysis is always focused on long-term outcomes. In some ways, the recent rise of ESG funds means it’s potentially too early to answer whether or not these funds have, indeed, delivered better outcomes. In order to answer this question, this analysis will focus on Australian-domiciled global equity funds, which are highlighted for two reasons: Global equities is the asset class containing the largest sample size of ESG funds available for Australian investors. Additionally, global equities provide the broadest possible investable universe of any asset class, so it is easier to analyse whether there are structural portfolio biases exhibited by ESG funds that may explain their performance characteristics.

Morningstar Direct data shows that there are 33 Australian-domiciled large-cap global equity funds with unique investment strategies that are tagged as sustainable investment funds. Only 19 of the 33 funds have a three-year track record, while just 14 of the 33 funds have a five-year track record as of 31 August 2021, which demonstrates how recent the growth in ESG funds is.

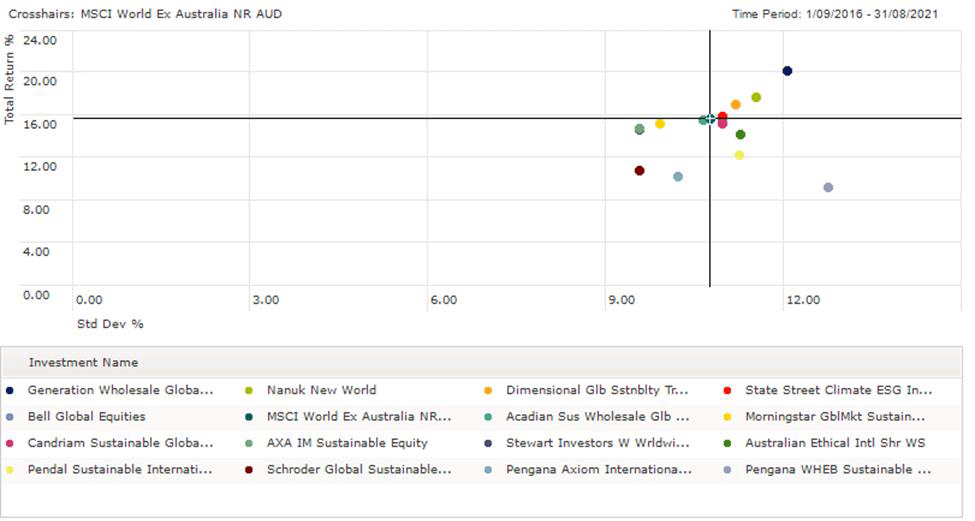

Using a simple risk/reward analysis in Morningstar Direct, the five-year return and standard deviation of each fund are compared and plotted on the following chart with the commonly used index for the asset class, MSCI World ex Australia, as the crosshair. The top-left quadrant (higher return with lower risk) is where every investor aims to be. As a comparison, Morningstar’s broadest global Sustainability index, the Morningstar Global Markets Sustainability NR Index, is included.

Exhibit 3: Australian sustainable funds; five-year return and standard deviation

(Click to enlarge) Source: Morningstar Direct

{kind=link}

This empirical evidence shows not a single one of the 14 ESG global equity funds available to Australian investors five years ago has been able to deliver a higher return with lower risk than the broad market index. Five funds (plus the Morningstar Global Markets Sustainability NR Index) have delivered lower return with lower risk over this period, five funds have achieved higher returns with higher risk, while four funds have delivered the double-whammy outcome of lower returns with higher risk than the index. Overall this isn’t a bad outcome, but nor is it a compelling investment outcome over this period.

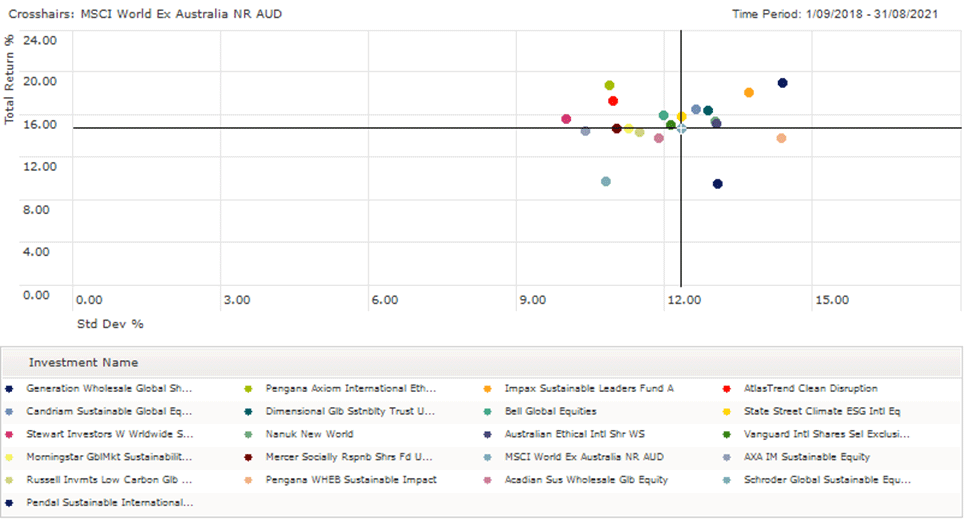

Results are more encouraging when looking at the same risk/reward analysis over the shorter three-year period, however.

Exhibit 4: Australian sustainable funds; three-year return and standard deviation

(Click to enlarge) Source: Morningstar Direct

{kind=link}

Seven funds (plus the Morningstar Global Markets Sustainability NR Index) achieved higher returns with lower risk than the MSCI Index, six funds had higher returns with higher risk, four funds delivered lower returns with lower risk, while just two funds had lower returns and higher risk.

What then is behind the recently improved outcomes for ESG funds? Are the funds that have launched in recent years been higher quality? Or has there been a structural move in markets that have helped ESG funds?

Portfolio composition of ESG funds

We have compared the realised return and risk of ESG funds with the broad market index, but what about the portfolios of ESG funds? Are there any structural differences in ESG funds that may explain this relative performance outcome?

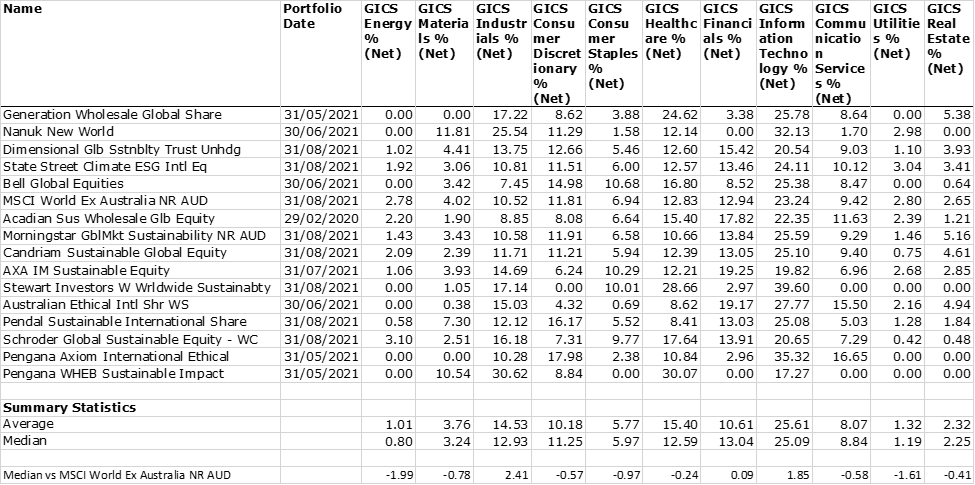

First, we look at the most recent portfolios of the 14 funds with a five-year track record, comparing their sector weightings against the MSCI World ex Australia Index.

Exhibit 5: Sector weightings

(Click to enlarge) Source: Morningstar Direct

{kind=link}

Overall, there aren’t huge differences between the median and average weights for each sector against the index. Mild overweights to information technology and industrials with underweights to energy and utilities aren’t a surprise for ESG-themed funds. There are individual outliers within the sample, like Stewart Investors’ healthcare and IT weights, but overall it appears that with sector exposures that don’t deviate wildly on average from the index, it’s no surprise that the returns don’t deviate too far from the index also.

What about underlying factor exposure?

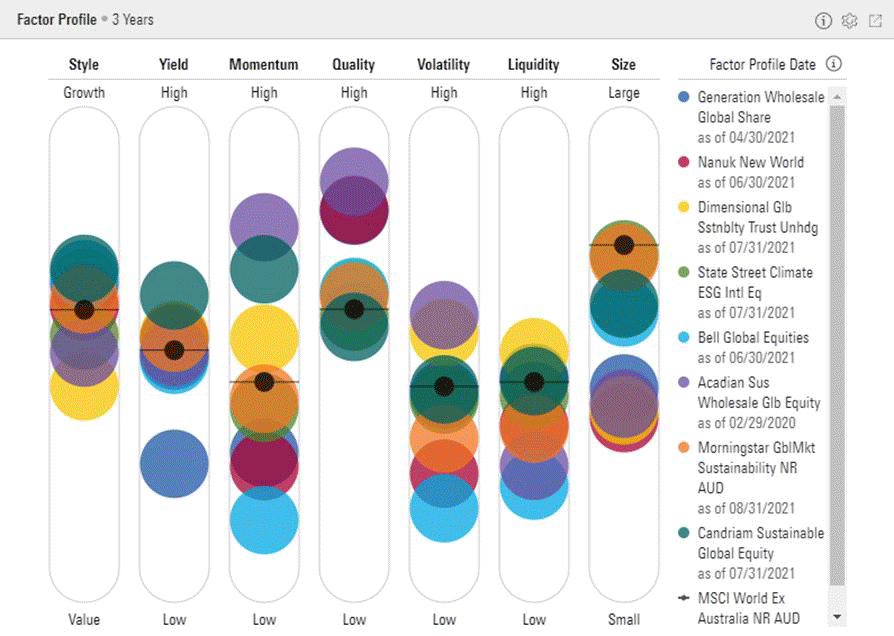

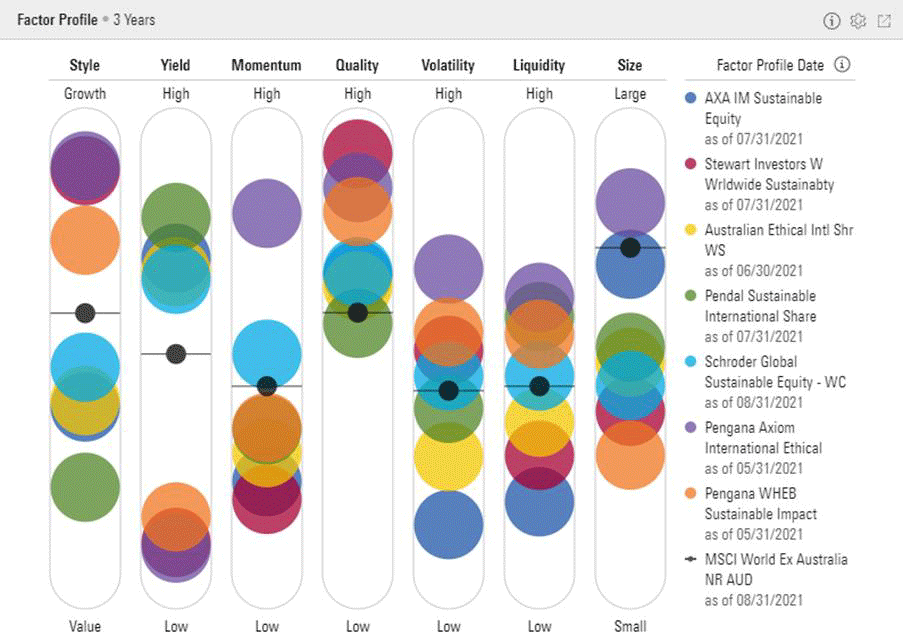

The holdings by sector don’t appear to be materially different to the index, but do the underlying factor exposures of the funds offer a different perspective? To analyse this, we used the Factor Profile tool within Morningstar’s Risk Model. The tool analyses portfolios across the following factors: Style, Yield, Momentum, Quality, Volatility, Liquidity, and Size. The tool handles up to 10 funds at a time, so the sample is divided into two charts as follows:

Exhibit 6 Factor profile

(Click to enlarge) Source: Morningstar Direct

{kind=link}

Exhibit 7 Factor profile

(Click to enlarge) Source: Morningstar Direct

{kind=link}

Each circle represents the relative factor exposure of the fund to the MSCI Index, which is the smaller black circle in each factor column. For most factors, there is a wide spread among different funds, without a noticeably different average. Some funds display a growth bias, others a value bias. The two systematic factor biases that stand out are the high-quality bias and the small-size bias. The small-size bias is not unusual for a sample of active funds, as most indexes, including the MSCI Index used here, tend to be large-cap-focused and therefore most active tilts tend to lead to a small factor tilt. The bias to the high-quality factor does appear to be a systematic bias of ESG funds in this sample. Only the Candriam, Pendal, and State Street funds exhibit lower than index exposure to the quality factor, and in each case, only marginally so.

Looking back at the characteristics of sustainable companies that these funds favour, the quality tilt isn’t surprising and aligns with the values of most ESG investment approaches. It does pose the question, though—are ESG funds just providing a quality tilt in disguise? Unflatteringly for the funds in this sample, if we were to add the VanEck MSCI ex Australia Quality ETF, an inexpensive global equity ETF with a purposeful tilt to the quality factor, which has been available on the Australian Securities Exchange since October 2014, it would be the second-best-performing fund over five years and the best-performing fund over three years. This apparent systematic bias of ESG funds to the quality factor is an important consideration when selecting funds for an overall portfolio.

Conclusions and implications for investment selection

The rapid growth of ESG investment options in recent years has increased the burden for fund selectors and investors who want to build ESG portfolios. The breadth of different approaches undertaken by funds, combined with differing methodologies for defining ESG, can make it very difficult to ascertain which funds are delivering an ESG proposition with merit for investment. We recently dealt with many of these issues in detail as we developed our methodology and then recently launched our own ESG model portfolios for advisors. Much of the analysis of portfolios, performance, and risk that are featured in this paper formed part of our assessment and selection criteria to build our ESG portfolios.

In many ways it’s still early days for ESG investing, as more money is allocated to the sector and differing investment approaches become available as the sector continues to evolve and mature. So far, the evidence is inconclusive that global equity ESG funds can improve returns or reduce risk, on average; but equally there is no evidence to suggest that ESG funds make these features worse. This is encouraging for investors who want to build ESG portfolios that align with their values, knowing that they shouldn’t have to sacrifice risk-adjusted return outcomes as a result. Having the right tools to appropriately analyse these investments and construct such portfolios is increasingly crucial in order to identify funds that are genuinely doing something different and worth paying for, while helping to skip over funds dressed up with an appealing ESG story that lacks substance when assessed under the hood.