Under the hood: Vanguard’s high yield ETF (VHY)

VHY consistently brings in high dividends but performance lags the ASX 200.

Mentioned: ANZ Group Holdings Ltd (ANZ), American Express Co (AXP), BHP Group Ltd (BHP), Berkshire Hathaway Inc Class B (BRK.B), Commonwealth Bank of Australia (CBA), Fortescue Ltd (FMG), The Kraft Heinz Co (KHC), Rio Tinto Ltd (RIO), Stt Strt SPDR S&P/ASX 200 ETF (STW), Stt Strt SPDR MSCI Aus Sel Hi Div YldETF (SYI), Vanguard Australian Shares High Yld ETF (VHY), Westpac Banking Corp (WBC)

When it comes to dividends, Warren Buffett likes to get, but not give. Berkshire Hathaway (BRK.B) has never paid a dividend in his 56 years in control. That's despite steady dividends from holdings such as Kraft Heinz (KHC) or American Express (AXP).

Buffett, with some justification, believes shareholder returns are better served by leaving the money with him.

“Our first priority with available funds will always be to examine whether they can be intelligently deployed in our various businesses,” he said in a 2012 shareholder letter.

“Our shareholders are far wealthier today than they would be if the funds we used for acquisitions had instead been devoted to share repurchases or dividends.”

But for the mere mortals who run most companies, dividends are a common way to return excess capital to shareholders. And for many investors in a low-interest rate world, dividends are a vital source of income.

So, in today's edition of Morningstar's Under the Hood, we look at the performance of Vanguard's Australian Shares High Yield ETF (VHY).

The fund collects a stable of blue-chip names with a history of high dividend yields. The Bronze-rated fund’s top 10 holdings averaged a 5.01 per cent dividend yield over the past five years.

Total returns are less impressive. VHY has lagged the ASX 200, with an annualised return over the past five years of 8.5 per cent, versus 10.78 for the index.

Still, the fund offers investors above-average equity income at low cost, says Morningstar manager research analyst Edward Huynh.

Picking dividend winners isn’t simple

VHY provides exposure to ASX companies with relatively higher forecast dividends. The ETF tracks the FTSE High Dividend Yield Index, which Vanguard has exclusive rights to.

In constructing a dividend index, providers screen for both dividends and their sustainability, says Elle Kuhta, a Morningstar Index product manager.

Providers want high dividend payers while avoiding “dividend traps”, whereby a high dividend yield obscures poor performance; perhaps management is paying out money that would be better spent investing in the business.

When the trap closes, investors are often left with a dividend cut and capital losses.

The index which VHY tracks screens companies based on the historical consistency and growth trajectory of dividends, as well as forecasts for dividends and their growth. It also screens for earnings per share as a measure of sustainability.

The approach penalises companies which pay sporadic dividends or whose dividends have been falling or are likely to fall.

Similar products like the SPDR® MSCI Australia Select High Dividend Yield ETF (SYI), or the Morningstar Australian Dividend Yield Index incorporate different sustainability metrics.

SYI includes leverage, while Morningstar uses the economic moat rating.

To ward off competitors, Vanguard has not disclosed the full set of rules it uses to construct its index, says Huynh.

“Unfortunately, this removes some transparency, one of the key attractions of passive strategies,” he says.

“That said, investors need not be overly cautious, as Vanguard has a long history of doing right by investors.”

Mixed long-run performance

VHY's performance has lagged the ASX 200, but outperformed similar product SYI.

VHY underperformed the ASX 200 on a total returns basis for six of the nine years between 2012 and 2020.

In the past year, VHY has edged ahead of the ASX, thanks to the rapid economic recovery that led a rotation to value last quarter. Total returns year-to-date are 2.73 per cent up on the index, and more than double SYI.

Annualised fund performance (month end data)

Source: Morningstar Direct

The Bronze-rated fund is the largest high dividend yield Australian ETF, with over $1.75 billion in net assets as of April. Net assets are nearly eight times larger than SYI.

The fund charges a management fee of 0.25 per cent, compared to 0.35 per cent for SYI. This puts it in the cheapest quintile of its Morningstar category.

A concentrated mix of household names

VHY’s 63 holdings are a highly concentrated, if consistent, set of dividend payers.

The top 10 holdings make up 69.36 per cent of the fund and are a who’s who of Australian blue chips: the big banks, the major miners, and Telstra, among others.

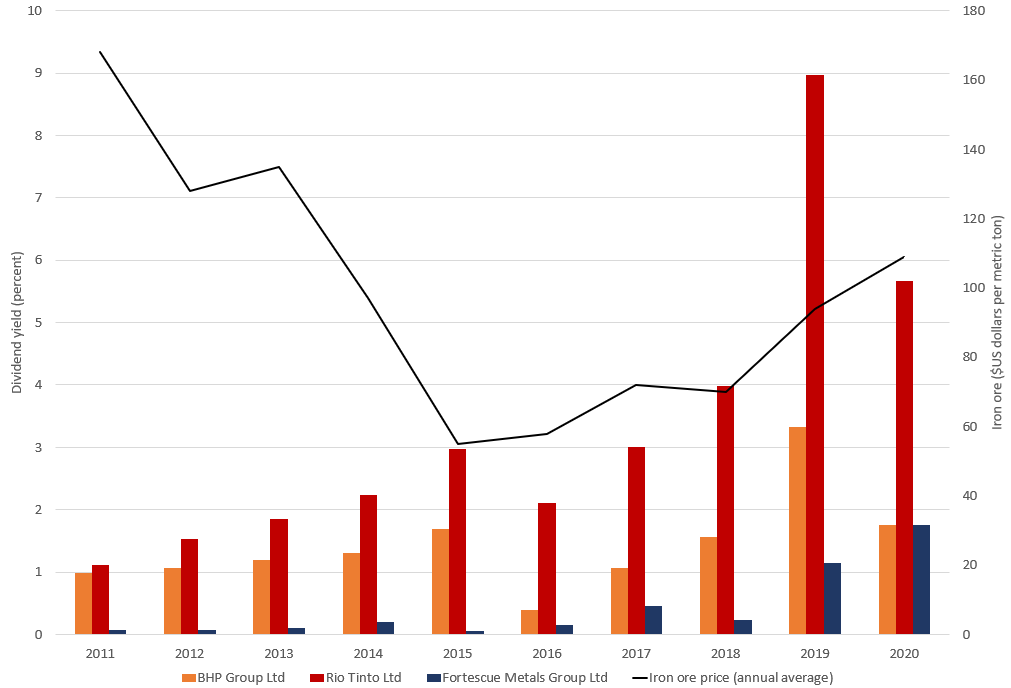

The big four banks, Rio Tinto (ASX: RIO), BHP (ASX: BHP), and Fortescue Metals Group (ASX: FMG) alone make up 52 per cent of the fund.

This result is sectoral skew to financials and basic materials, which make up 65.6 per cent of the fund.

This exposure helps explain its underperformance versus the ASX 200, says Huynh.

“Poorly timed buys into materials such as BHP and Rio Tinto hurt in 2016,” he says.

“Vanguard recouped some of these losses in 2017, though this was curtailed as exposure to Telstra took a bite out of returns.

“As the banking industry came under pressure because of falling property prices and the focus of the Royal Commission in 2018, returns were again below the broader market.”

Source: Morningstar Direct, Statista

Consistent dividend performance

Dividend performance has been strong. The five-year average dividend yield across the holdings is 4.04 per cent, compared to 2.17 per cent for the SPDR S&P/ASX 200 tracking ETF, STW.

Eighty-three per cent of the holdings paid a dividend each of the past five years and only five stocks haven’t paid a dividend in the past twelve months.

Top 10 holdings and dividend performance

Data as of May 26, 2021

Source: Morningstar direct

A high proportion of economic moats

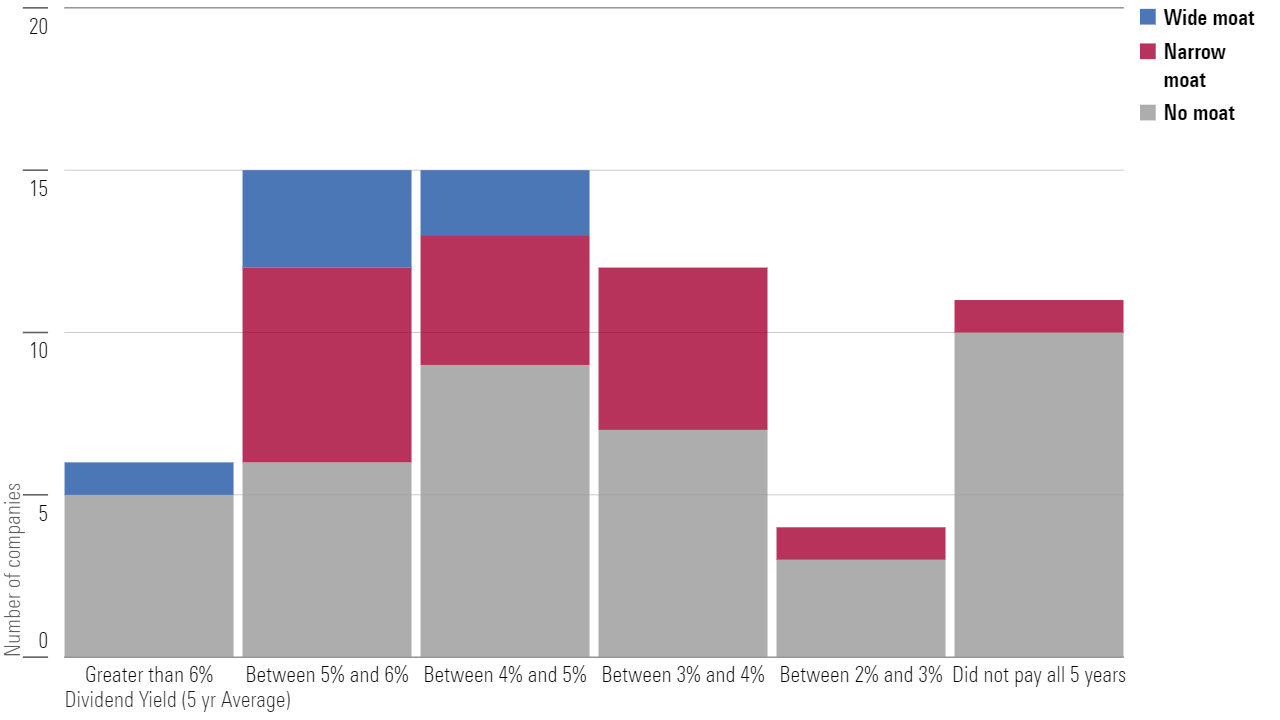

Comparing the dividend track record of VHY to the Morningstar moats gives an indication of sustainability.

VHY’s holdings have a higher proportion of wide moats, which imply a 20-year competitive advantage, than the broader universe of ASX companies Morningstar covers.

Ten per cent of VHY’s holdings have wide moats, versus 7 per cent for the coverage universe.

The holdings with the highest historic yields often have economic moats.

More than half of the companies which paid more than a 5 per cent average dividend yield over the past five years had wide or narrow moats.

Source Morningstar Direct

Looking ahead, forward dividend yields are high, although few companies are trading at discounts to their Morningstar fair value estimate.

Of the top 15 holdings by portfolio weight, seven have a forward dividend yield greater than 4 per cent. None are trading at discounts to their Morningstar fair value estimate.

Seven of the top 15 holdings have a forward dividend yield greater than 4

Source: Morningstar Direct

Blue chips aren’t term deposits

The days of comfortably living off government bonds coupon payments are long over, and today’s low-interest world is forcing many investors to search for new strategies for reliable income.

At first glance, blue-chip dividends look like ideal substitutes for the term deposits and high-grade fixed interest of old, but investors are exposing themselves to capital losses, says Morningstar editorial director Graham Hand.

In a downturn, companies cut dividends and investors are left with less income and a capital loss. Covid led ANZ (ASX: ANZ) and Westpac (ASX: WBC) to suspend dividend payments for the first time in decades. The Commonwealth Bank (ASX: CBA) must deal with billions in remediation charges associated with the banking royal commission.

The big miners, which make up 20 per cent of VHY’s holdings, are vulnerable to fluctuations in commodity prices.

Hand says investors have a third option: using capital when necessary. Vanguard's Aidan Geysen makes a similar point in a Firstlinks piece from 2020.

“Where an income-oriented strategy utilises returns as income and preserves capital, the total-return approach encourages the use of capital when necessary,” he says.

Ultimately, CBA dividends are probably a more reliable bet than holding Afterpay (ASX: APT), but that doesn't mean they are without risk.